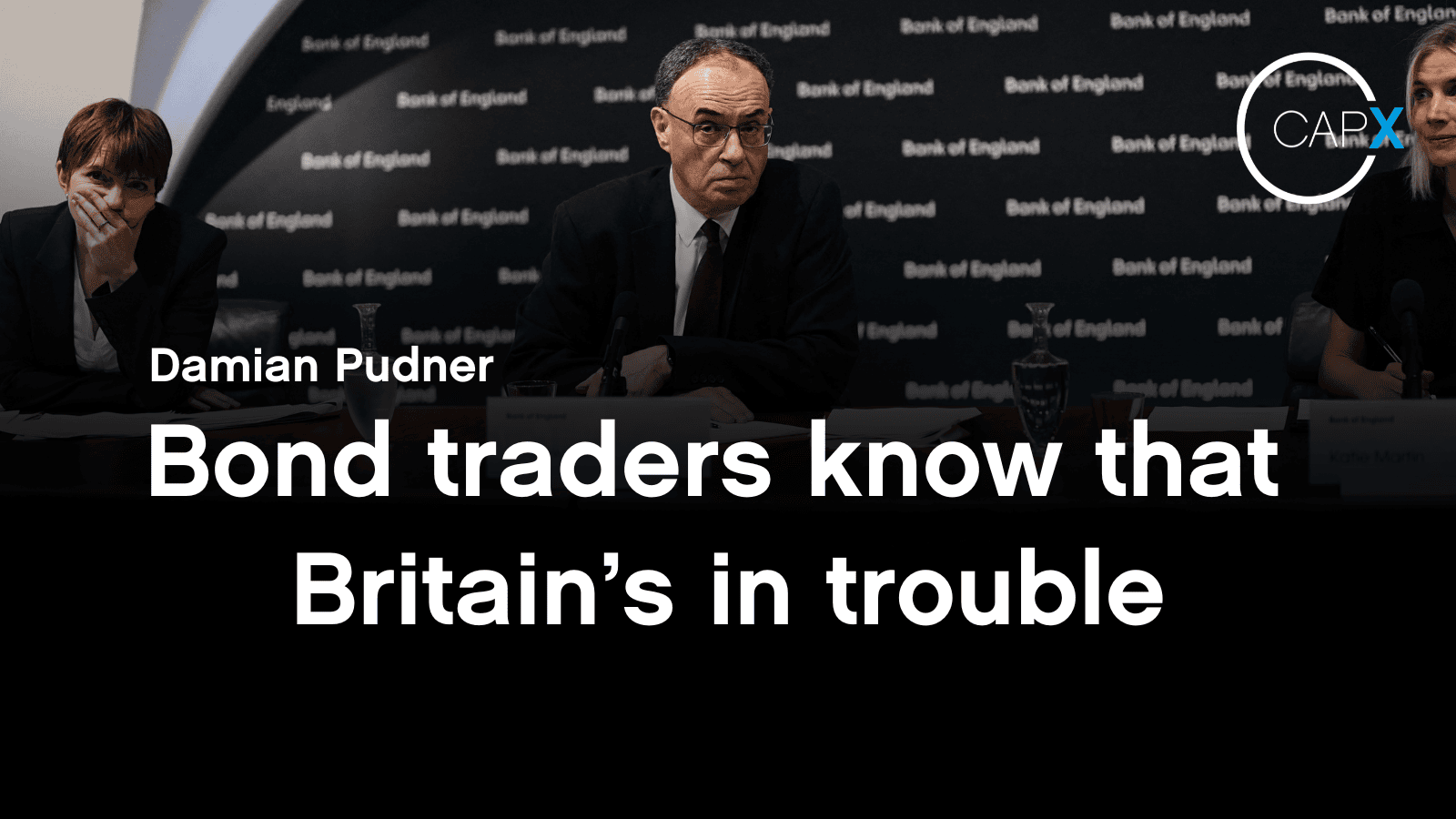

Last Thursday, the Bank of England pulled off a remarkable feat: it cut interest rates and still managed to spook the markets. The Monetary Policy Committee scraped through a 5–4 majority for a quarter-point cut to 4%, only succeeding on a second attempt. One member, Alan Taylor, had initially argued for twice as much. The gilt market’s instant response? Drive borrowing costs up.

It was pure ‘Yes, Prime Minister’. Governor Andrew Bailey, looking and sounding like a civil servant dispatched to defend a policy he didn’t fully believe in, mumbled through a press conference that inspired neither clarity nor confidence. His deputy, Clare Lombardelli, sat beside him with the look of someone desperate to be elsewhere. The bond markets muttered ‘oh dear’ – and promptly dumped gilts.

And yet – incredible though it may sound – the decision itself was right. It’s just that the Bank managed to turn a necessary rate cut into a communications calamity.

I know I’m in the minority, but I’ll say it: the Bank must go further. Yes, it’s contrarian with inflation still above target, but that doesn’t make it wrong. Today’s better-than-expected 0.3% GDP growth for the second quarter flatters a decelerating economy after a tariff-driven surge at the start of the year. Without that quirk, the picture is far bleaker, as this week’s dire jobs data and gloomy forward-looking business surveys confirmed.

Unemployment, already at a four-year high of 4.7%, is still climbing. Vacancies are vanishing. Wage growth, on broader measures, is losing momentum. Two more rate cuts before the end of the year are needed, even if inflation nudges up to 4% this September, as the Bank expects, to head off a grinding stagnation that will only make it harder to service our debts.

Of course, even doves must acknowledge the danger of cutting rates while inflation still runs hot. Services inflation and wage growth remain uncomfortably high. June’s CPI figure of 3.6%, driven by energy and food prices, £25 billion in NIC hikes and a 6.7% jump in the national living wage, is awkward for those of us urging looser policy. But this isn’t 2021. Fears of returning to a post-Covid-style price surge are misplaced. Demand is already weak, and tax rises in the Autumn Budget will weaken it further. Business investment and confidence are on life support, consumer sentiment barely better. The greater danger continues to be chronic lack of meaningful and sustainable growth, and that, not just inflation, should be shaping monetary policy.

The Bank’s narrow remit makes matters worse. Its primary mandate is to keep annual inflation at 2%. But if it no longer delivers growth and prosperity, why cling to it? Why not give the Bank a dual mandate to explicitly include growth? Better still, why not a nominal GDP target? Monetary policy needs the flexibility to respond to a faltering economy.

Which brings us to fiscal dominance: when interest rates are set with one eye permanently on the Government’s burgeoning debt. Britain’s £2.8 trillion of debt is more fragile than it looks, increasingly owned by flighty hedge funds and overseas investors. A quarter of it is inflation-linked, and quantitative tightening forces the Treasury to find new buyers at much less forgiving rates. It’s a dangerous mix.

This is where monetary policy collides with political reality. Without serious spending restraint, the Bank will remain a prisoner of fiscal weakness. Whoever’s in power – Labour today, the Conservatives or even Reform UK tomorrow – will find the bond market an unforgiving mistress.

The state must shrink – radically, permanently and starting now. That means reforming the triple lock before it bankrupts the next generation. Ending the pretence that public sector pensions can remain gold-plated while private pensions wither. Cutting the Civil Service by 25%, and meaning it, not promising a ‘bonfire of the quangos’ while quietly adding kindling. Ending welfare for those perfectly capable of work and restoring the principle that support is for the genuinely needy.

And we have to stop treating the NHS as off-limits. No more blank cheques for ever-longer waiting lists. Tie funding to outcomes: waiting times, survival rates, productivity. Strip away the layers of unnecessary bureaucracy. Publish productivity scores for the Civil Service – and remove staff who fail to meet the grade. Cap public spending at 40% of GDP, forcing politicians to prioritise instead of pretending they can promise everything to everyone.

If we want growth, we must rediscover the spirit that once made Britain the world’s most dynamic economy. Rip up the planning system. Slash the regulatory jungle strangling business and enterprise. Treat entrepreneurs and investors as the lifeblood of recovery, not villains to be taxed, lectured and driven abroad. Overhaul and simplify the tax system entirely. Why not one flat rate of income tax, corporation tax cut to 15% and stamp duty and inheritance tax abolished? An unapologetic message that Britain rewards work, welcomes investment and is open for business again.

This is the radical reset Britain needs. The irony is that it may fall to an ideologically left-wing government to deliver reforms usually associated with the Right – the sort of changes the last Conservative government, in its caution and centrist drift, ducked entirely. If Keir Starmer and Rachel Reeves want to avoid presiding over a prolonged economic slump, they’ll have to govern more like Margaret Thatcher than Tony Blair.

The politics are brutal. The Civil Service – our modern-day Sir Humphrey – will counsel against it. ‘Minister,’ they’ll murmur, ‘this policy would be extremely courageous.’ In Whitehall, that’s code for ‘political suicide’. But, as one great visionary warned, ‘What’s the alternative? To go on as we were before? All that leads to is higher spending. And that means more taxes, more borrowing, higher interest rates more inflation, more unemployment.’

Last week’s cut was supposed to ease pressure. Instead, it exposed it. When gilt yields rise after a rate cut, the bond market is sending a blunt message: it isn’t fooled by token gestures. Without serious reform, future cuts will be read not as confidence, but as bailouts for a bloated, unreformed state.

So yes, I’ll keep making the unfashionable case for deeper, faster cuts. But unless they’re paired with the most far-reaching spending reforms in a generation – to reset and shrink the state – monetary policy will remain captive to fiscal decay, and Britain’s decline will go from possible to inevitable.

The choice for Starmer and Reeves – and for every government after them – could not be starker: govern like Jim Hacker, forever deferring to Sir Humphrey’s instinct for inaction, or heed the real voice of reason – the bond market – and make the hard choices to put Britain back on course to sustainable growth and economic stability.

As Sir Humphrey might put it: ‘Prime Minister, the ship of state is listing badly. We can patch it here and there – but if you truly want to save it, you’ll have to take the helm and change course.’ For once, the bond market would applaud.

– the best pieces from CapX and across the web.

CapX depends on the generosity of its readers. If you value what we do, please consider making a donation.

Columns are the author’s own opinion and do not necessarily reflect the views of CapX.