As property tax bills have risen rapidly across the state, property tax reform has moved to the forefront at the General Assembly. Among the policy options under consideration are levy limits, which restrict the annual growth rate of total property tax revenue.

Unfortunately, the discussion has been marred by misconceptions that levy limits would force cuts to local government budgets or prevent revenues from keeping pace with rising costs and growth. However, levy limits do not require local governments to reduce their existing budgets and, when well-designed, allow revenues to increase with inflation and population growth.

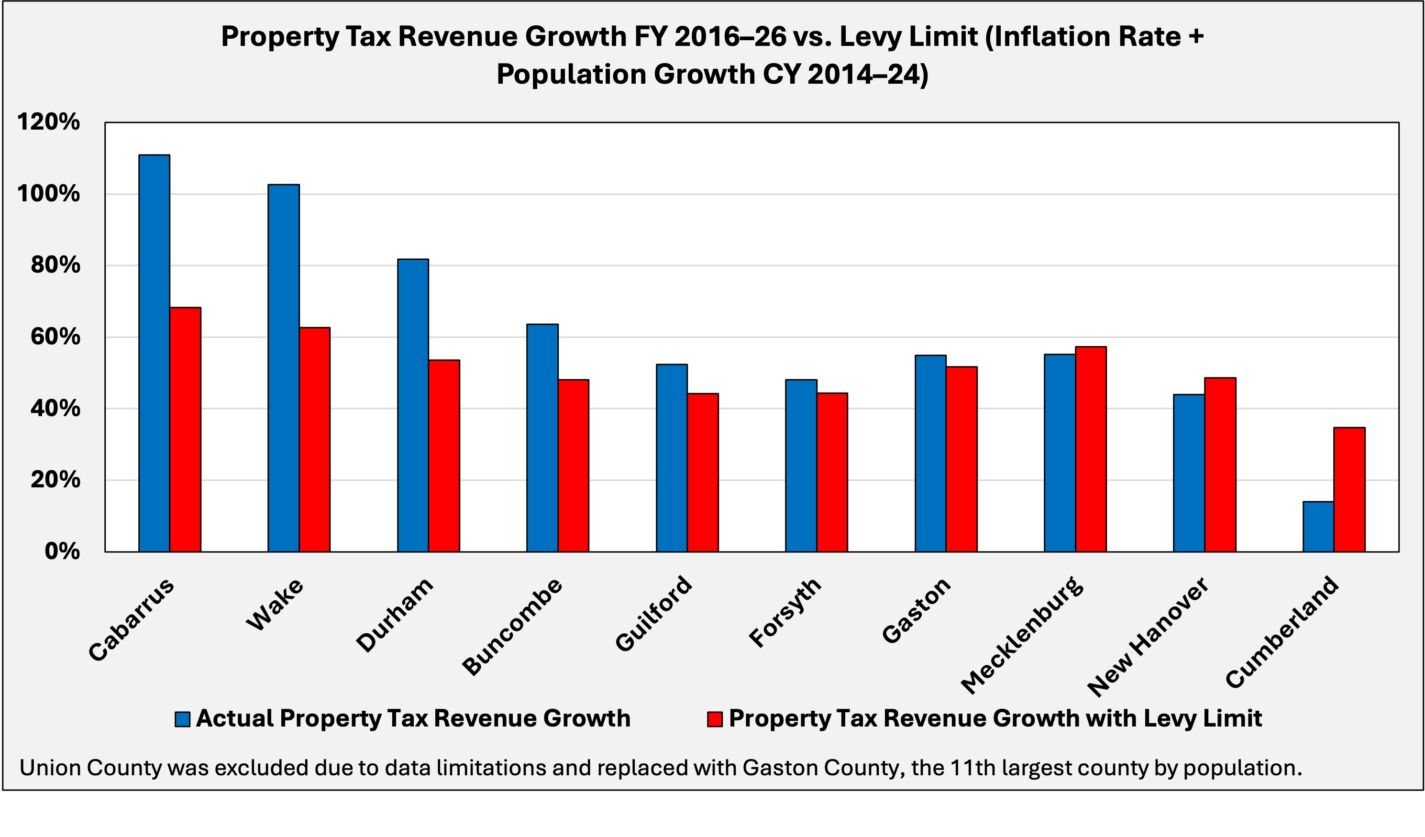

This article aims to provide clarity by examining how property tax revenues in the state’s 10 largest counties have grown over the past decade, relative to a hypothetical benchmark that limits property tax revenue growth to inflation plus population growth. (see methodology below)

Summary results

Across the counties examined, property tax collections exceeded inflation plus population growth by roughly $2.7 billion over the past decade.

However, the results vary widely by jurisdiction. Some counties saw property tax revenues grow far faster than the benchmark, while others remained close to, or even below, it. On average, county property tax revenues increased 63 percent, while the levy limit benchmark would have allowed 51 percent growth.

County-by-county results

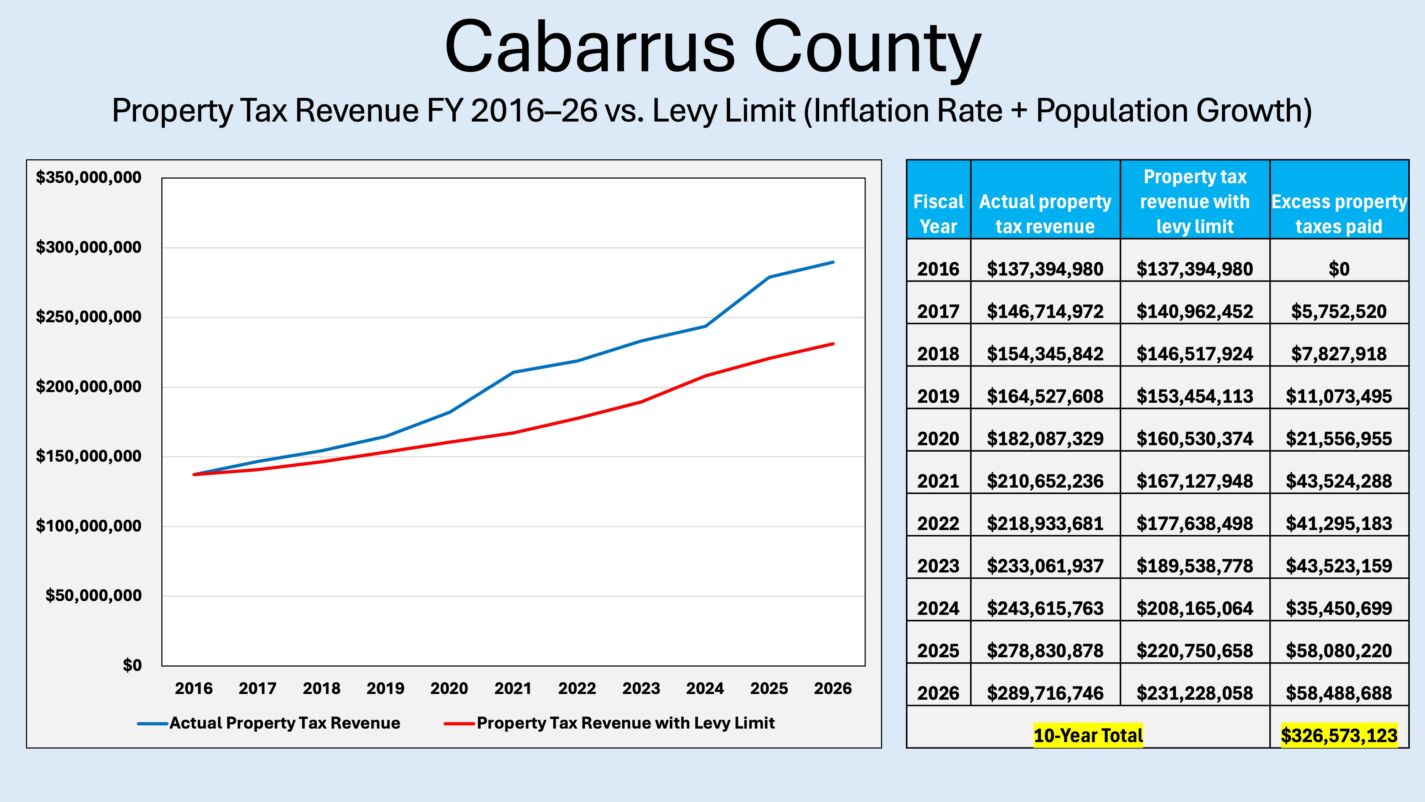

Cabarrus County experienced the largest gap between actual property tax revenue growth and the levy limit benchmark. Property tax collections increased by 111 percent, compared with 68 percent under the benchmark. Over the decade examined, this resulted in roughly $326.6 million in additional property taxes paid than would have been under the levy limit.

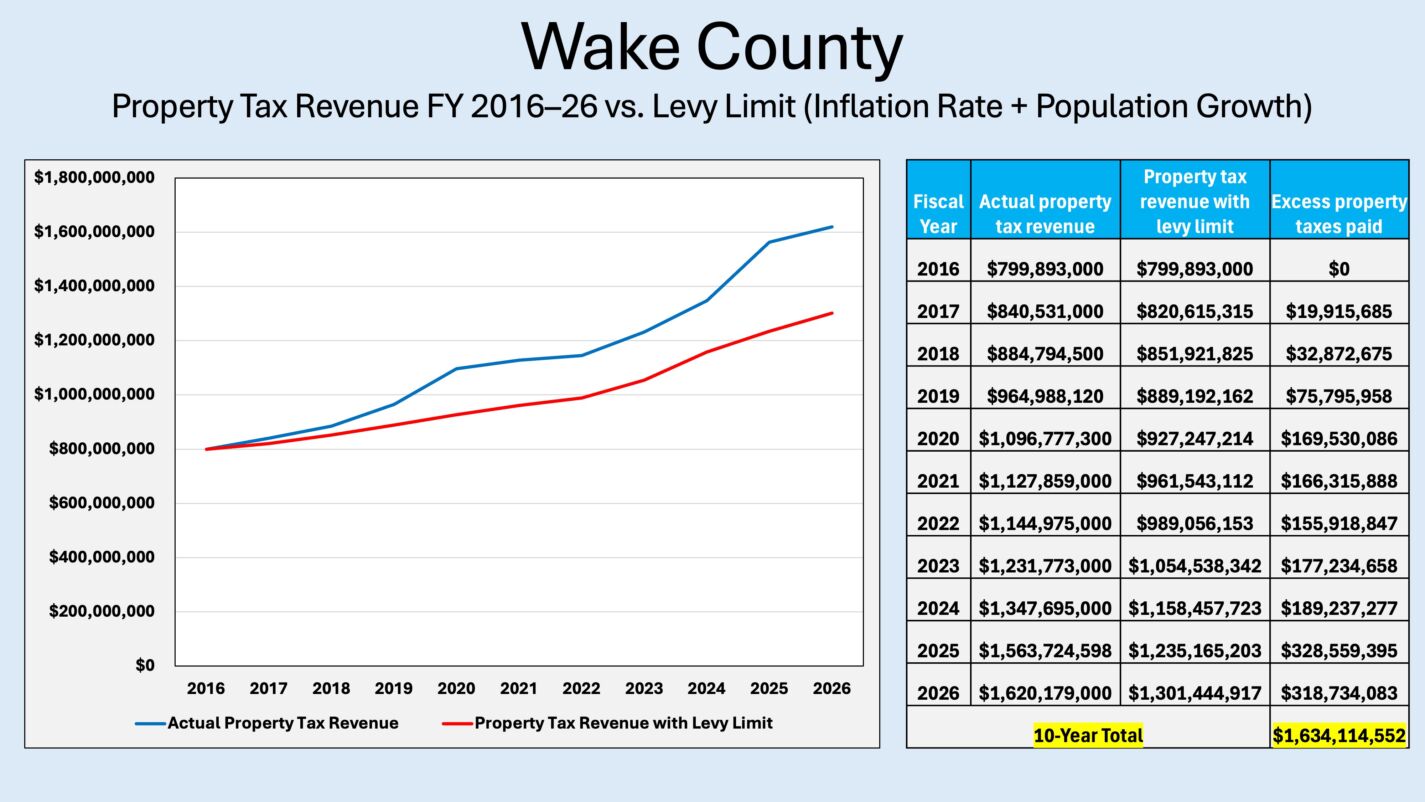

Wake County experienced the second-largest gap between actual property tax revenue and the levy limit benchmark. Property tax collections grew by 103 percent, compared with 63 percent under the benchmark. Over the past decade, this difference resulted in roughly $1.63 billion in additional property taxes paid than would have been under the levy limit.

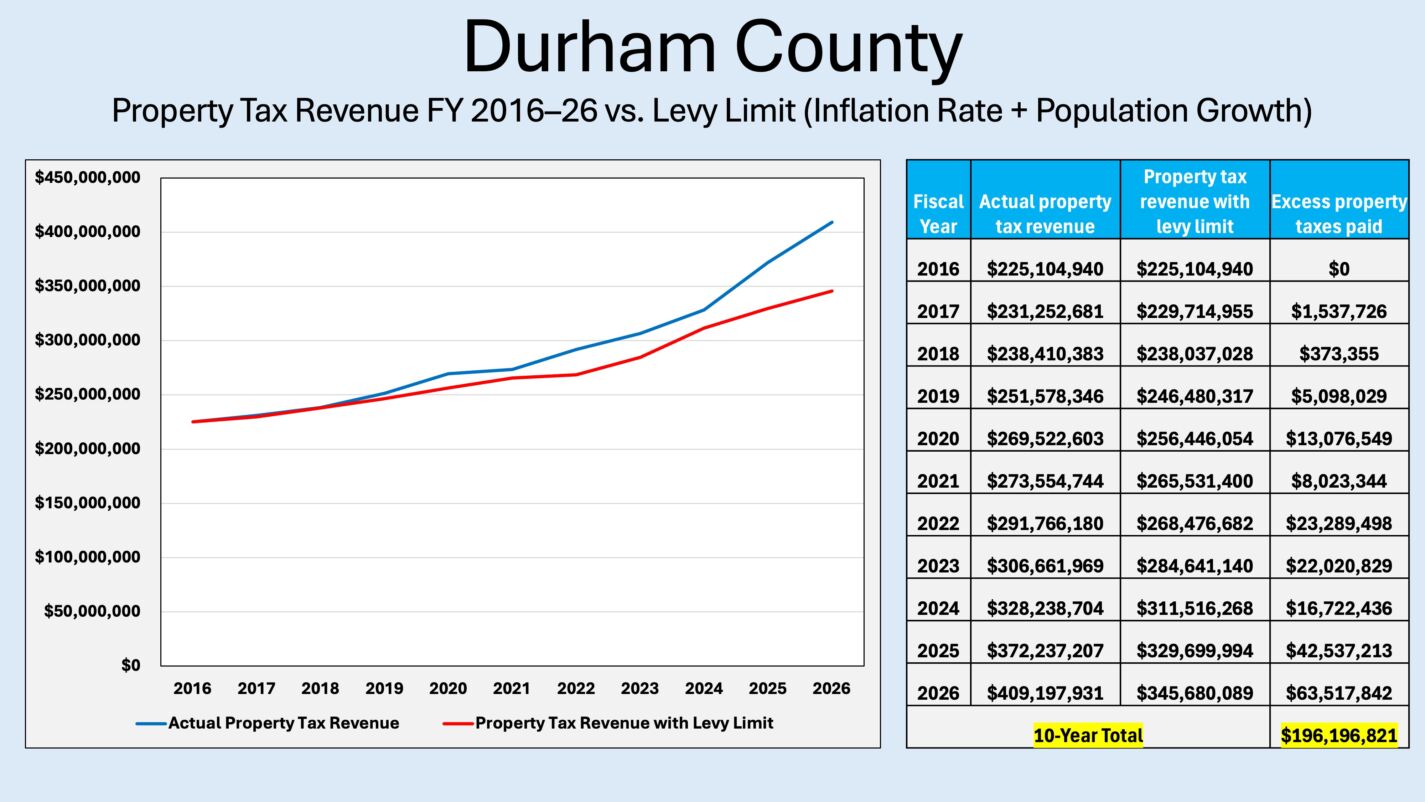

Durham County experienced the third-largest gap between actual property tax revenue and the levy limit benchmark. Property tax collections increased by 82 percent, compared with 54 percent under the benchmark. Over the past decade, this difference resulted in roughly $196.2 million in additional property taxes collected above the levy limit.

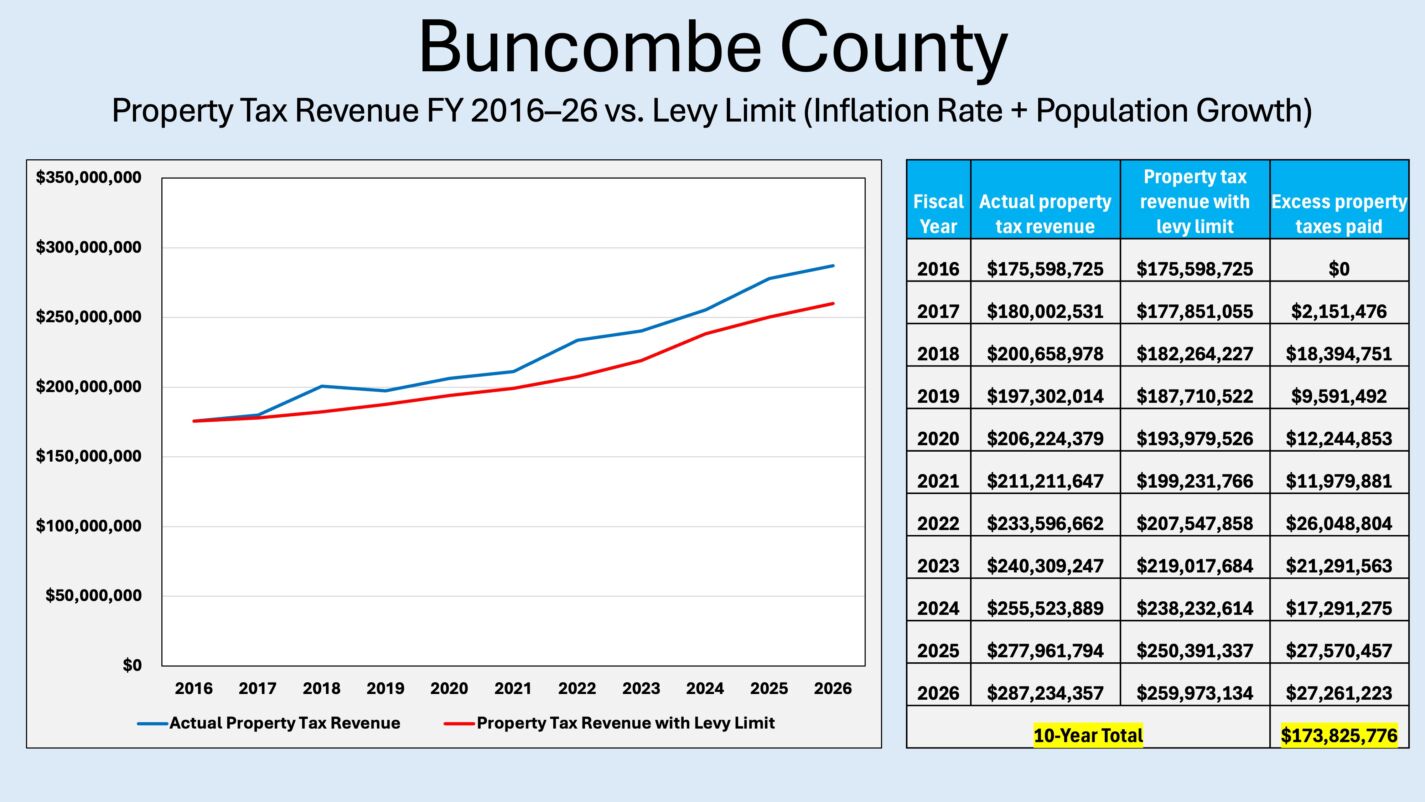

Buncombe County’s property tax revenue grew substantially faster than the levy limit benchmark. Property tax collections increased by 64 percent, compared with 48 percent under the benchmark. Over the decade, this difference resulted in roughly $173.8 million in additional property taxes collected above the levy limit.

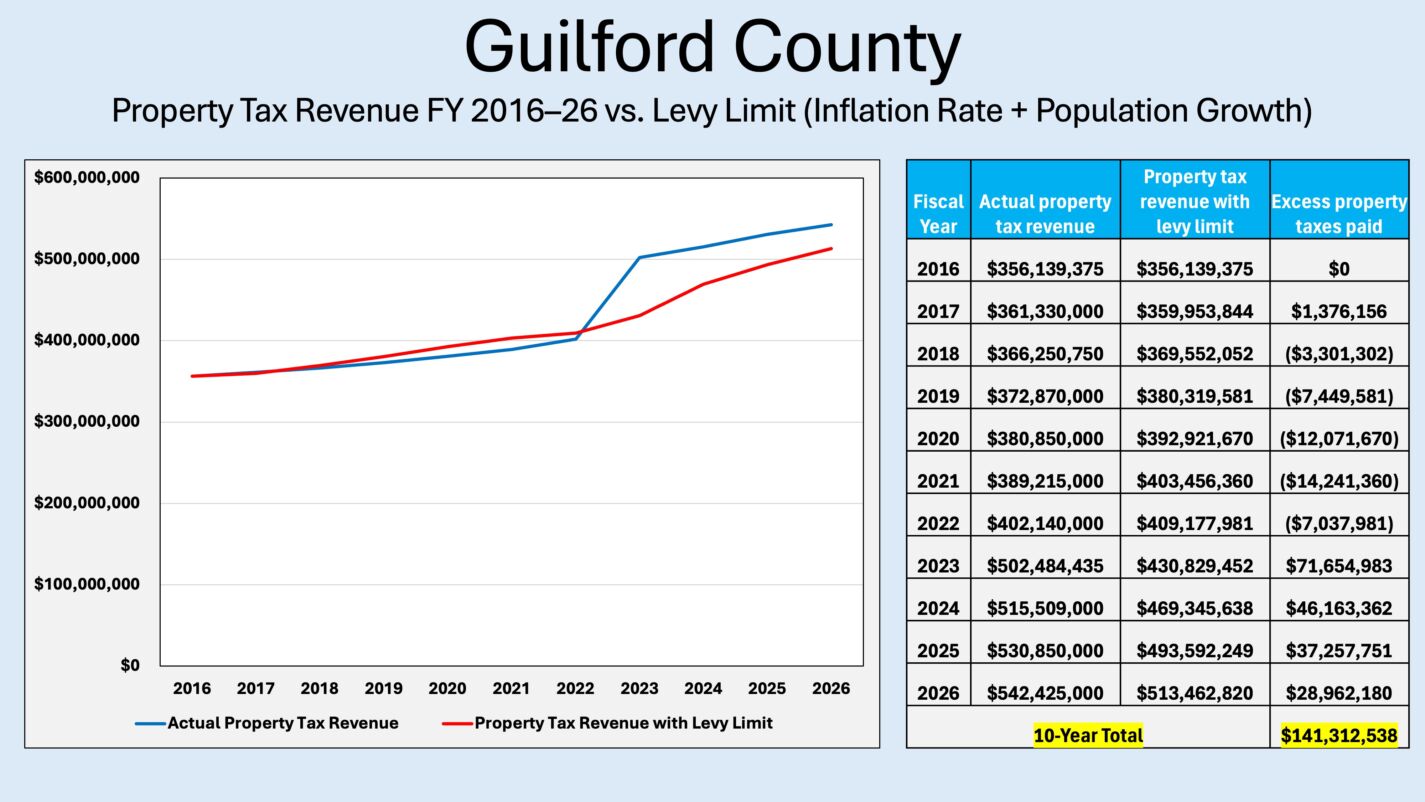

Guilford County’s property tax revenue grew moderately faster than the levy limit benchmark. Property tax collections increased by 52 percent, compared with 44 percent under the benchmark. Over the decade, this difference resulted in roughly $141.3 million in additional property taxes collected above the levy limit.

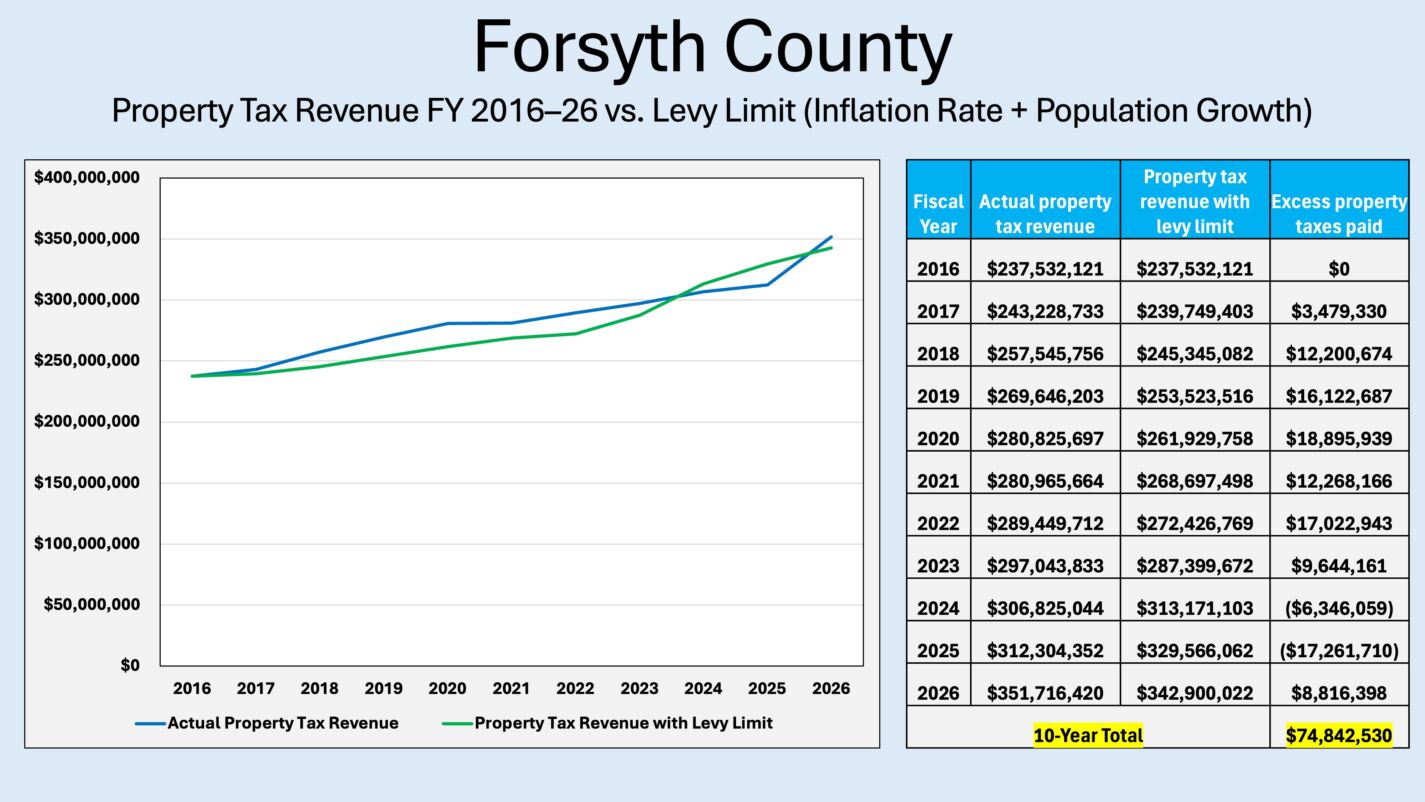

Forsyth County’s property tax revenue grew slightly faster than the levy limit benchmark. Property tax collections increased by 48 percent, compared with 44 percent under the benchmark. Over the decade examined, this resulted in roughly $74.8 million in additional property taxes collected beyond the levy limit.

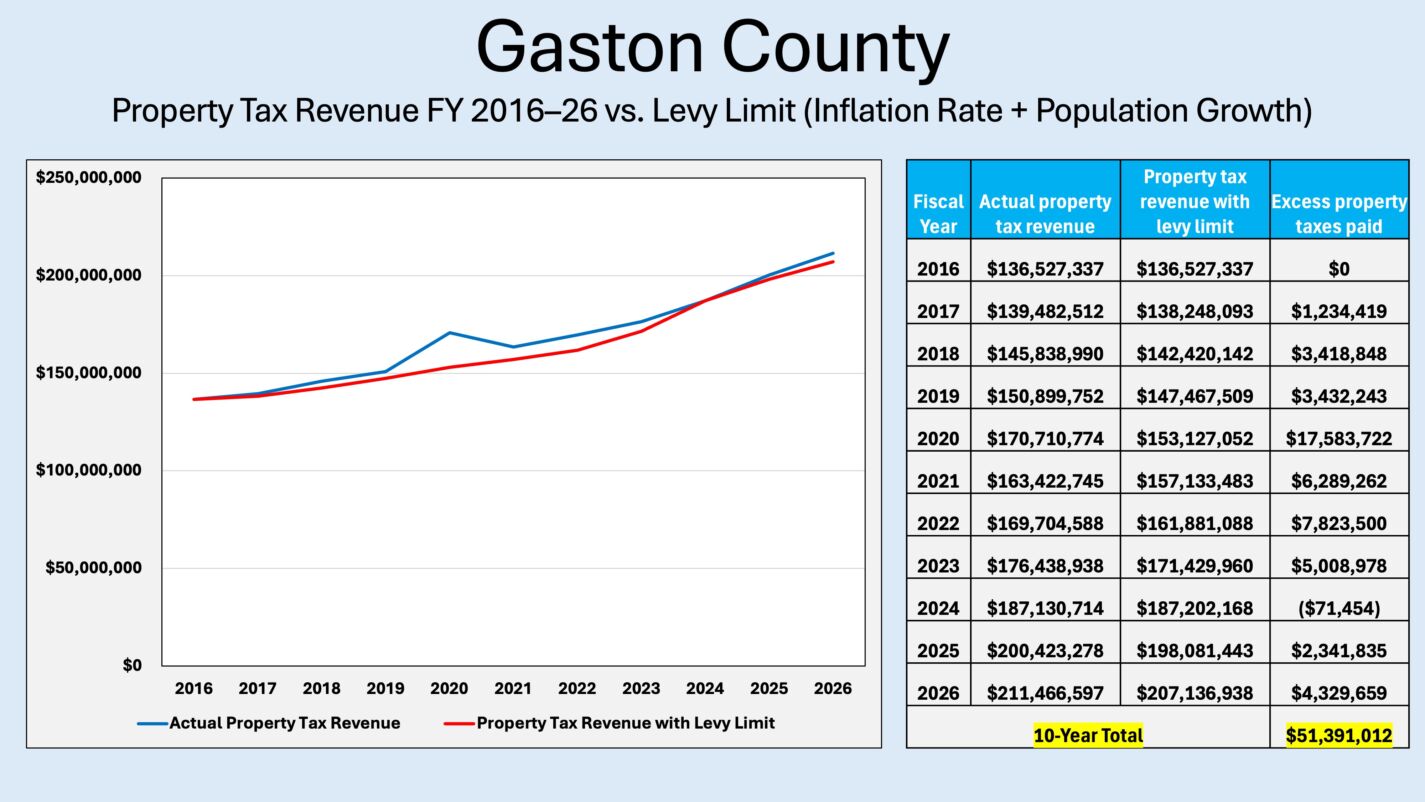

Gaston County’s property tax revenue grew slightly faster than the levy limit benchmark. Property tax collections increased by 55 percent, compared with 52 percent under the benchmark. Over the decade, this difference resulted in roughly $51.4 million in additional property taxes collected above the levy limit.

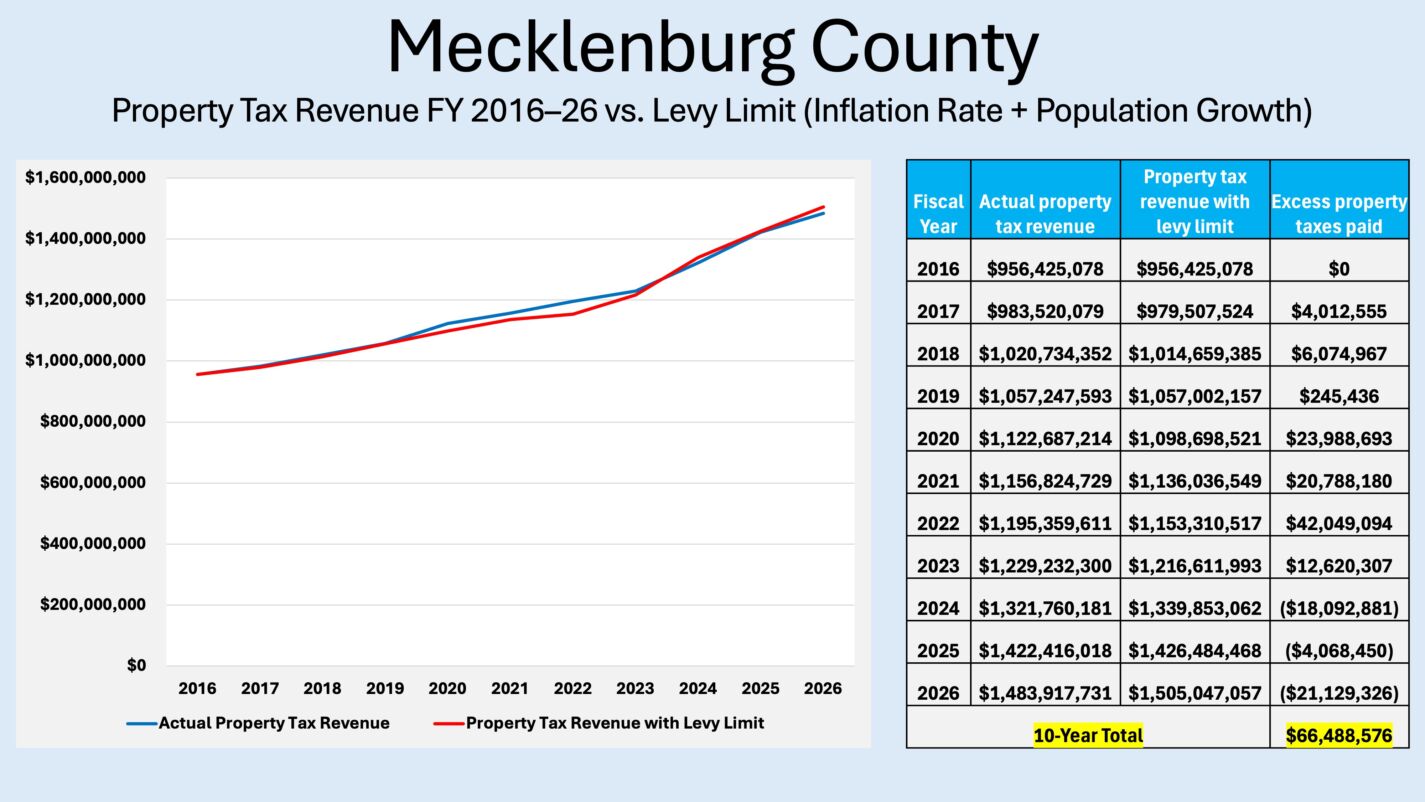

Mecklenburg County’s property tax revenue growth closely tracked the levy limit benchmark. Property tax collections increased by 55 percent, compared with 57 percent under the benchmark. However, because collections exceeded the benchmark in several earlier years, the county still collected roughly $66.5 million more over the decade than it would have under the levy limit.

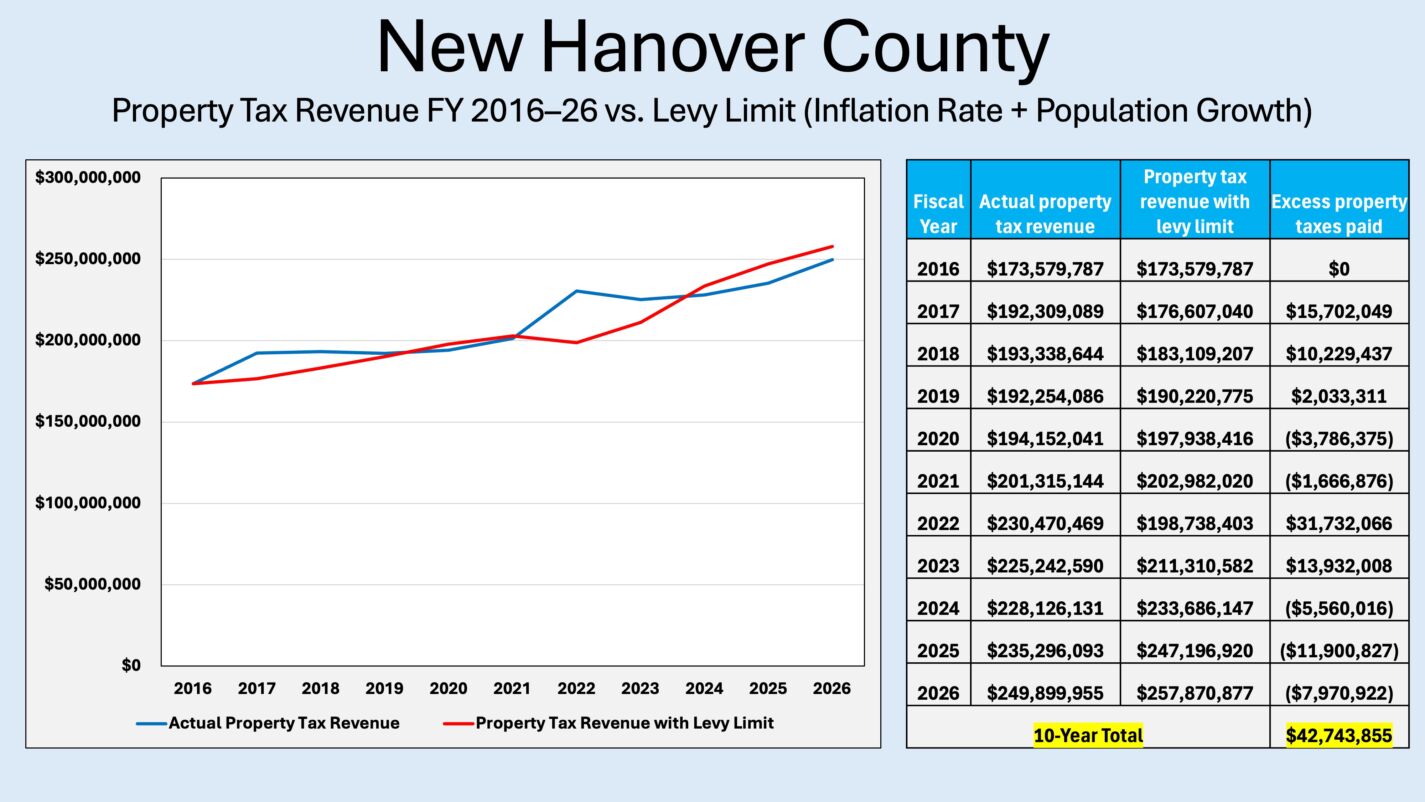

New Hanover County’s property tax revenue growth was generally close to the levy limit benchmark. While revenue increased by 44 percent, compared with 49 percent under the benchmark, the county still collected about $42.7 million more in property taxes over the decade than it would have under the levy limit.

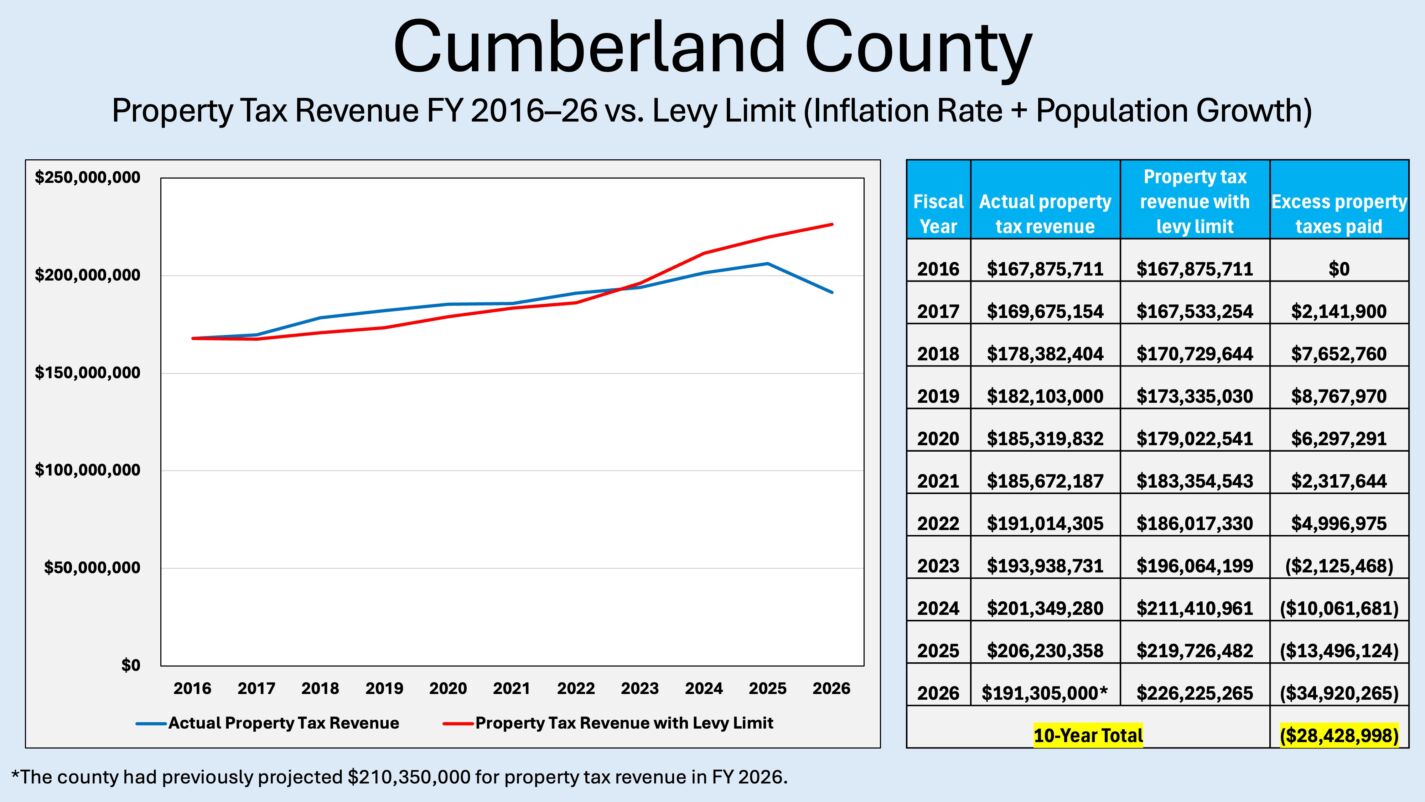

Cumberland County’s property tax revenue grew well within the levy limit benchmark. Property tax collections increased by only 14 percent, compared with 35 percent under the benchmark, meaning taxpayers paid about $28.4 million less than they would have if the county raised property taxes the full amount allowed under the levy limit.

Other considerations

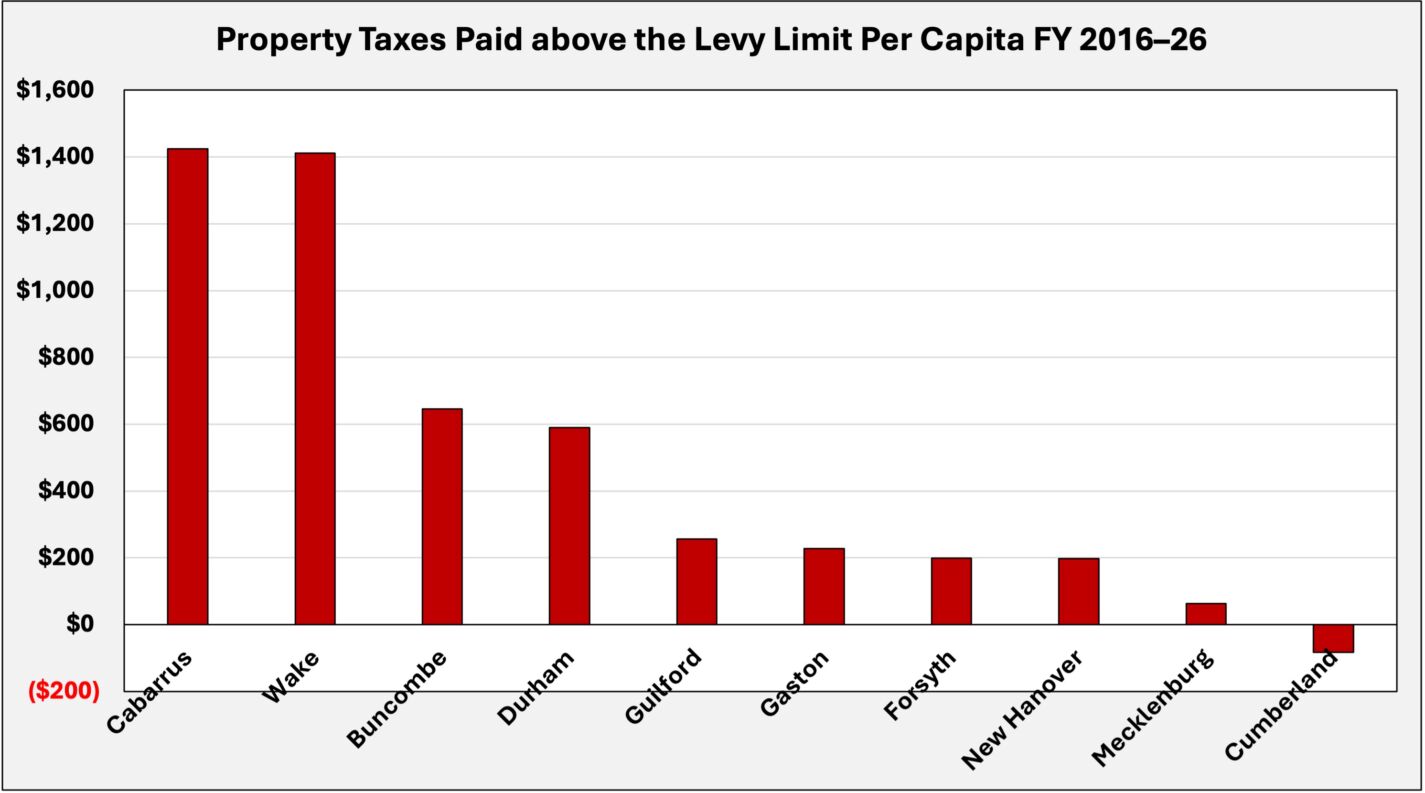

Looking at property taxes paid above the levy limit on a per capita basis can help to illustrate the long-term impact on residents.

Counties such as Cabarrus, Wake, Buncombe, and Durham stand out for collecting substantially more in property taxes per resident than would have been the case under the levy limit. Guilford, Gaston, Forsyth, and New Hanover also exceeded the benchmark, though by more modest margins.

Meanwhile, Mecklenburg and Cumberland kept property tax revenue growth close to, or below, the benchmark, reflecting comparatively strong fiscal discipline.

While this analysis approximates the revenue effects of a levy limit, implementing such a policy would also require several important design decisions.

- First, counties would need to conduct annual property revaluations and collect reliable new-construction data, which would provide a more accurate measure of tax base growth than population.

- Second, policymakers should consider adopting a zero-percent inflation floor to prevent revenue reductions during periods of deflation while still allowing negative adjustments when population declines.

- Third, lawmakers must determine whether the levy limit should apply only to real property or to all categories of taxable property.

- Finally, policymakers must decide whether such limits should apply only to county governments or to all property taxing jurisdictions.

Closing thoughts

Levy limits are not budget cuts. They simply place guardrails on how quickly property tax revenues can grow in the future, allowing counties to keep pace with inflation and population while preventing excessively rapid expansions in tax collections.

As this analysis shows, many counties would have little to worry about under such a policy. Jurisdictions such as Mecklenburg, Cumberland, and New Hanover already kept revenue growth close to the benchmark.

However, counties such as Wake, Cabarrus, Durham, and Buncombe would not be able to continue increasing property tax collections as aggressively as they did over the past decade, which is precisely the behavior levy limits are designed to restrain.

Methodology

This analysis compares actual county property tax revenue growth from fiscal year (FY) 2015–16 to FY 2025–26 with a hypothetical levy limit tied to inflation plus population growth. Property tax revenues were collected from county budgets, and while county revenue structures varied, the data used are consistent over time within each county.

Inflation was measured as the percentage change in the annual average Consumer Price Index from 2014 to 2024, while population growth was measured as the percentage change in the county population over the same period. These rates were applied annually and compounded to produce the allowable revenue path.