“The Bottom Line: The latest draft of Senator Galt’s BI-11 would deliver modest but meaningful ongoing property tax relief for every existing property owner, and more substantial long-term relief now that it has mostly closed the voted-levy loophole.”

The following has been adapted from an excerpt of the Frontier Weekly Newsletter written by Cole Koenig for the April 2nd edition.

We’ve been getting a lot of questions from readers about BI-11, the ballot initiative to cap property taxes proposed by Senator Wylie Galt last week. How impactful would it actually be?

We released an initial statement on the draft last Thursday and have since updated our analysis because the draft has been revised. Here’s a copy of the latest version we’ve seen:

Let’s break it down.

We think BI-11 is focused on the right thing: directly limiting the growth of government.

The Cap: As currently drafted, we think BI-11’s property tax cap would deliver modest but meaningful ongoing tax relief for every existing property owner.

BI-11 would replace the current cap on local property tax revenue growth in 15-10-420 MCA with a hard 2% per-parcel per-year constitutional cap on the amount of taxes levied on individual existing property owners.

This subtle difference would deliver three main benefits:

- More predictable, and generally slower, ongoing annual tax growth for all existing owners, because increases are locked at a fixed 2% rather than fluctuating with the inflation.

- Stronger protection from big valuation-driven tax spikes, because local governments must set the mill levy low enough to ensure the total taxes paid by each existing owner rises by no more than 2%, even when property values surge.

- Reduces uneven tax shifting during reappraisals, because the mill levy must be adjusted down to enforce no more than 2% increase per parcel. This protects fast-appreciating properties from absorbing a disproportionate share of the tax burden.

The Voted Levies: The original draft kept the current loophole that allows local govs to bypass Montana’s property tax cap through a simple majority of voters in an election. We noted this was a missed opportunity to provide more substantial tax relief because voter-approved levies are a major driver of the property tax burden.

The graph below presented to the Governor’s Property Tax Task Force is a good illustration of this. The blue line is actual local gov property tax revenues from 2015-2023 and the orange line is the estimated authority for non-voted taxes under the 15-10-420 MCA cap. The blue line exceeds the orange line by $100M due mainly to tax hikes that voters approved in excess of the cap:

I’m happy to report that the latest version of BI-11 has mostly closed this voted-levy loophole. The draft now requires a majority of all registered voters, not just votes cast in an election, to increase property taxes above the 2% cap. This change significantly raises the bar for passing voter-approved tax levies, which will provide more substantial ongoing relief.

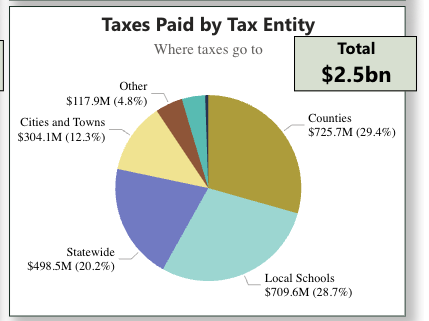

The Scope: It’s important to level-set the expectations here with readers. BI-11 only addresses property taxes from local governments, which account for only ~40% of property tax bills. BI-11 DOES NOT address taxes going to K12 schools, which are ~55%+ of property taxes paid. Limiting local government property taxes is important but it’s only one part of the picture. Here’s a quick snapshot for 2026:

The Bottom Line: The latest draft of Senator Galt’s BI-11 would deliver modest but meaningful ongoing property tax relief for every existing property owner, and more substantial long-term relief now that it has mostly closed the voted-levy loophole. It would also provide more predictability and less volatility due to valuation changes. If this is the final draft, Frontier Institute will happily support BI-11.

While BI-11 would be a step forward addressing local government property taxes, we continue to believe in the long run Montana needs fiscally conservative limits on the growth of state, school, and local budgets to address the root cause of taxation.

For Liberty,

Cole Koenig