Michigan ranks 16th on the Tax Foundation’s State Tax Competitiveness Index. Ranking in the top third is fairly good, but Michigan’s trajectory is not. The state ranked 11th only five years ago and has been sliding ever since. While other states improve their tax competitiveness, Michigan is standing still.

It was at risk of dropping even further when advocates of the Invest in MI Kids campaign started a drive to add five percentage points to the rate paid by the state’s top earners. The campaign’s organizers say they will delay their target from the 2026 general election to the 2028 election.

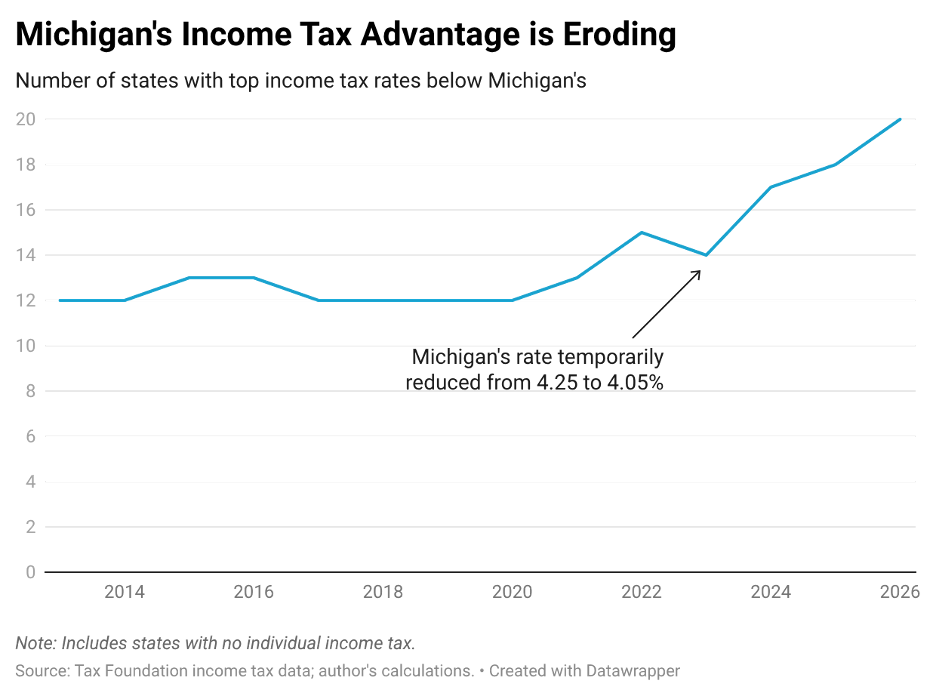

Twenty-six states have cut income tax rates over the past five years, and 23 of those have cut their top rates. Michigan reduced income tax rates for 2023, but the 4.25% rate resumed the next year after the governor concluded that the revenue trigger that caused the rate cut should be only temporary.

While 18 states had top income tax rates below 5% in 2021, the numbers stands at 27 today, and 20 have rates below Michigan’s 4.25%.

Twenty years ago, only four states, including Michigan, had a single-rate income tax. Five years ago, there were seven. Today Michigan is one of fifteen states with a single-rate income tax.

Michigan’s low, single-rate income tax, along with a regionally competitive sales tax, is a major reason why it is in the top third of the State Tax Competitiveness Index. In last year’s ranking, however, Michigan tumbled from 14th to 19th overall on individual income taxes. The index, of course, is just a measure, and a rank is just a number. But that rank represents something real. Tax competition is ramping up, and states that rest on their laurels — or worse, surrender some of their competitive edge — risk slower economic growth and job creation.

States’ tax trajectories are diverging. Most states are cutting income tax rates, reforming their tax codes, and emphasizing greater competitiveness, but a few are doubling down on high rates. Within a 24-hour window, lawmakers in Washington approved legislation that will soon impose a 9.9% tax on the income of high earners, while South Carolina legislators passed a bill intended to phase out the state’s income tax entirely, subject to revenue availability. Those two actions are a microcosm of the emerging divide.

Income taxes fall on labor and investment. High income tax rates cut into economic growth, and a strong and economically important impact will fall on small businesses. Higher rates will affect their propensity to invest, their ability to expand, and the number of people they employ.

Economic studies consistently show that high income tax rates are a drag on states’ economies. A Tax Foundation analysis estimated that a 9.25% top rate in Michigan — as called for in the recently paused “Invest in MI Kids” campaign — would cost an estimated 43,000 jobs, cut wages by about 1%, and shrink the state’s economy by $8.5 billion.

One of the virtues of a flat tax is that it keeps marginal rates in check. Economic decision-making takes place at the margin; the tax rate on the next dollar of income is the tax rate that matters most. When states must tax all income at the same rate, this exerts downward pressure on that rate. This is a major reason why Colorado’s income tax rate is 4.4%, Illinois’ is 4.95%, Pennsylvania’s is 3.07%, and Michigan’s is 4.25%, despite political pressures in each state that would likely yield much higher marginal rates if graduated-rate structures were permitted.

Michigan could take many steps to improve its tax climate. Immediate expensing of business machinery and equipment purchases would avoid penalizing capital investment, which current tax law does. Raising filing and withholding thresholds would ensure that nonresidents aren’t required to file and remit taxes to the state for visiting for a single day. Reforming the unemployment insurance tax regime could create greater stability, moving away from the current system, under which tax burdens increase dramatically during an economic downturn, when businesses struggle to avoid further layoffs.

Michigan’s property taxes are too high, moreover, and its property tax system needs reform. The state’s assessment limits, for instance, reduce tax burdens on some properties by shifting them onto others — particularly new homes and structures, and those purchased by first-time homebuyers. This discourages new construction, exacerbating housing affordability and increasing the cost of starting a business. Michigan should pursue better ways to keep property tax burdens in check.

But if there’s one certain way Michigan could lose its competitive standing, it would be to abandon its low, flat-rate income tax.

Businesses and individuals are more mobile than they were during the COVID pandemic. The rise of remote work gives individuals more choices in where to work. It also gives employers more flexibility. They can locate in many more places, knowing that even if their qualified workforce is not completely in place, they can fill some roles remotely.

And as more states enhance their tax competitiveness, the list of options expands, making it easier to live, work, invest, or locate one’s business in a low-tax state. For all their advantages, Florida and Texas aren’t for everyone. But with a growing number of states offering a competitive tax environment, the prospects of a good fit increase dramatically, and the costs of states disregarding tax competitiveness rise accordingly.

Michigan and its regional peers face stiff economic headwinds, while other states, particularly in the Sunbelt and the Mountain West, experience robust economic and population growth. Lawmakers in Lansing can’t control every factor contributing to these dynamics. But they can shape the state’s tax code in ways that will either attract residents and spur economic growth, or turn away both. They’ve received a reprieve, for now, from the effort to make things worse. It’s time for them to act.