As the 2026 legislative session wound down, it looked as though Republicans wouldn’t be able to agree on one of the party’s signature issues: cutting business taxes. During committee of conference negotiations last week, word spread (and was even reported in the news) that a House-passed Business Enterprise Tax cut was dead.

House and Senate negotiators, however, did strike a compromise. Proposed by Rep. Joe Sweeney, R-Salem, the agreement addresses Senate concerns about potential revenue losses by building multiple revenue triggers and safeguards into future BET rate cuts.

Called the Business Enterprise Tax, the BET might better be called the Business Existence Tax. “Business enterprise” in statute is defined as an “organization engaged in or carrying on any business activity within this state,” except for tax-exempt non-profits.

The BET is a tax on “the sum of all compensation paid or accrued, interest paid or accrued, and dividends paid by the business enterprise.”

Businesses don’t have to earn a profit to owe BET payments, which makes it particularly irksome for smaller businesses that generate enough revenue to pay.

The committee of conference version of House Bill 155 breaks BET reduction into two parts.

- It raises the filing threshold from $250,000 of gross business receipts to $400,000. The Department of Revenue Administration (DRA) estimates that this would exempt an additional 4,500 businesses from BET liability. Because the DRA is required to adjust the threshold for inflation, the current filing threshold is $298,000, rather than the statutory $250,000.

- It sets into place automatic BET rate cuts of 0.05 percentage points only if four conditions are met:

- Combined business tax revenue from the BET and Business Profits Tax is at least $100 million above budget, net of refunds, at the end of a state fiscal year.

- Combined business tax revenue is above the prior fiscal year.

- Combined General Fund and Education Trust Fund revenue is at or above budget.

- The state rainy day fund is at or above its statutory cap.

When the BET was created in 1993, the rate was set at 0.25%. Of course, initial tax rates never stay low for long. Just seven years after the BET was created, legislators had tripled the rate to 0.75%.

Starting in 2015, lawmakers began to bump the rate down to its current 0.55%. Rep. Sweeney’s goal is to bring the rate back down to its original level.

HB 155 would do this by triggering a reduction of 0.05 percentage points every time the state budget generates a $100 million business tax surplus and the other three safeguards are met.

For HB 155 to bring BET rates back to their 1993 levels, all four revenue metrics would have to be met in six separate fiscal years.

In the last decade, all conditions were met only five times, in Fiscal Years 2022, 2021, 2019, 2018 and 2016. That does not mean that the conditions would have been met if HB 155’s provisions had been in effect at the time.

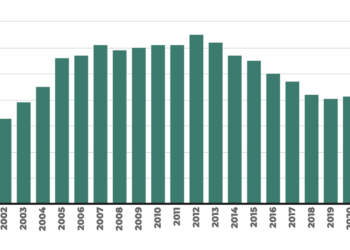

Business tax revenues vs. plan by year:

- 2025: Below plan by $163.4 million

- 2024: Below plan by $21.3 million

- 2023: Above plan by $300 million * Total revenues were below prior year

- 2022: Above plan by $260.9 million

- 2021: Above plan by $217.2 million

- 2020: Below plan by $85.3 million

- 2019: Above plan by $151.6 million

- 2018: Above plan by $118.8 million

- 2017: Above plan by $72.7 million

- 2016: Above plan by $132.8 million

The compromise version of HB 156 is an example of New Hampshire building on its own successes. In 2015, legislators negotiated a package of business tax cuts that included rate reductions tied to a General and Education Trust Fund revenue target, which the state later hit.

The revenue triggers in HB 156 are much more difficult to achieve than the single number set in 2015. They ensure that business tax revenues must be above plan and above the prior year before a BET rate cut can take effect. And that rate cut would be small, just 0.05% at any one time. No BET rate cut could occur if either business tax revenues or total General and Education Trust Fund revenues fell below budget.

In short, no BET rate cut would occur unless state revenues were stable and business tax revenues were growing.

HB 156 represents an extremely cautious approach to trimming business tax rates. But building certainty into future rate cuts can add to the New Hampshire Advantage. These automated rate cuts, even with the challenging triggers, signal to current and prospective business owners that investments in New Hampshire will be rewarded with lower tax burdens. If they grow their businesses here, and that growth leads to higher state revenues, they’ll be rewarded with smaller tax bills.

As “tax-the-rich” fever continues to spread through the Northeast, this offer—lower tax rates for increased investment—will make New Hampshire an even more attractive place to start or grow a business.

For context, below is the Department of Revenue Administration’s own chart showing the annual change in business tax revenues over the last decade.