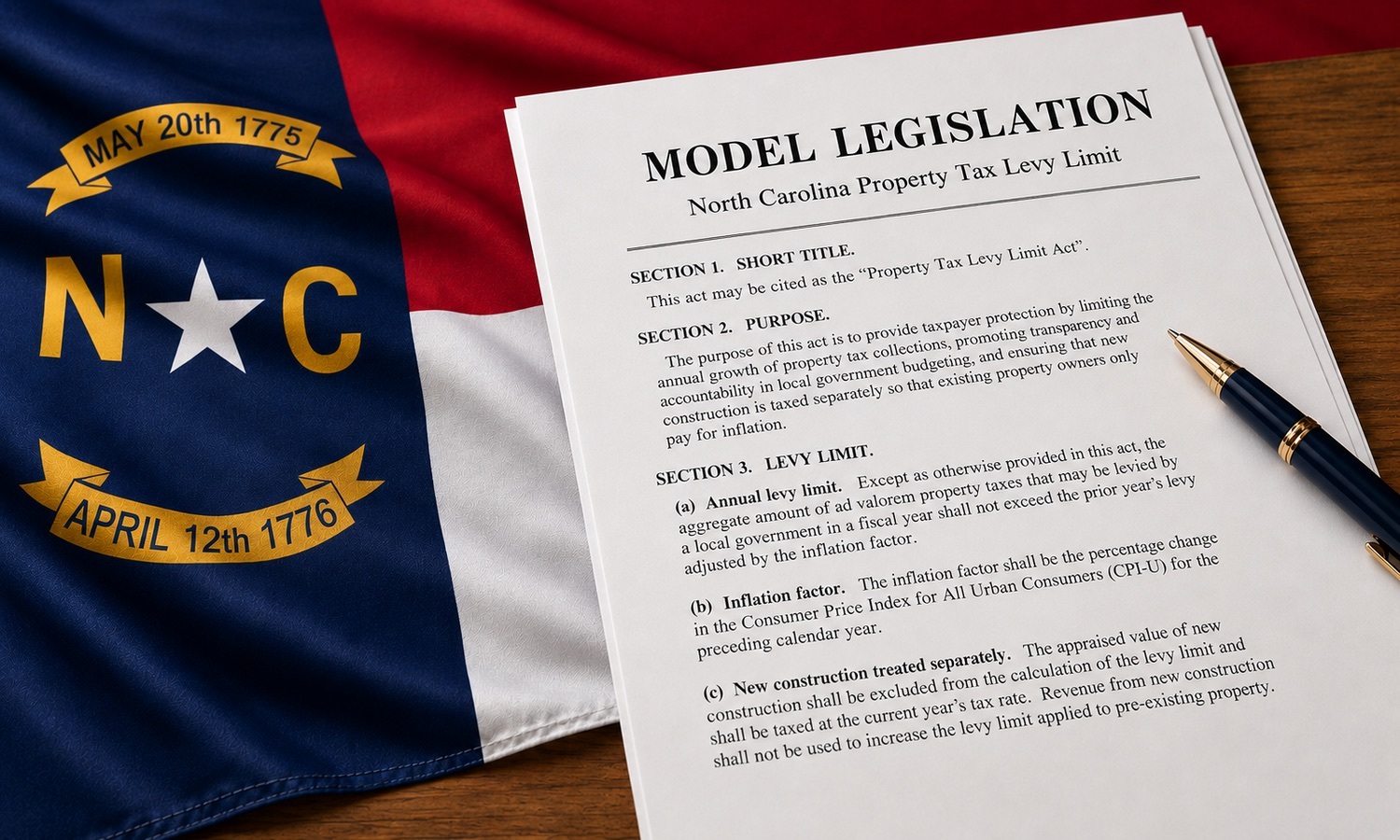

House Bill 1089 has quickly intensified North Carolina’s growing debate over property tax reform.

After months of discussion within the House Select Committee on Property Tax Reduction and Reform, the proposed constitutional amendment received the required three-fifths supermajority support in both chambers of the General Assembly. North Carolina voters will now decide whether to adopt the amendment on the November ballot.

The amendment would require the state legislature to establish a levy limit capping the growth rate of local property tax collections.

Critics argue that a levy limit could reduce local government flexibility and undermine public services. Supporters, meanwhile, point to years of property tax collections that, in many localities, have exceeded inflation and population growth, arguing that stronger taxpayer protections are needed.

A key feature is that the constitutional amendment would only require the state legislature to “enact general laws limiting the amount by which the levy of taxes on property may increase, which may include exceptions.”

It doesn’t define the formula to which the increases would be tied.

Why isn’t the formula in the amendment?

Naturally, one might question why the formula is not explicitly defined within the constitutional amendment itself. That concern is understandable.

However, levy limits are inherently more complex than, say, a simple tax rate cap and require policymakers to address a wide range of technical questions, including inflation adjustments, population growth, override mechanisms, and the treatment of exceptions.

For that reason, it is likely wise for the constitutional amendment to establish the broader principle of taxpayer protections while allowing accompanying legislation to define the specific mechanics of the policy. Embedding every operational detail directly into the constitution would make future adjustments far more difficult.

Allowing accompanying legislation to define those details provides greater flexibility and enables policymakers to adapt the formula when fiscally appropriate.

That approach preserves the broader constitutional protection for taxpayers while avoiding the rigidity that can result from permanently constitutionalizing highly technical fiscal formulas.

Core characteristics of a well-designed levy limit

A poorly designed levy limit could create unnecessary fiscal strain, encourage loopholes, disconnect local government revenues from economic growth, or fail to provide legitimate protection to taxpayers.

A well-designed levy limit, however, can provide meaningful taxpayer safeguards while still allowing local governments to grow alongside their communities.

At its core, a well-designed levy limit should remain tied to economic realities, treat new construction separately from existing properties, include minimal exceptions, and allow for voter-approved overrides. The long-term success or failure of a levy limit in North Carolina will ultimately depend on how policymakers balance those four principles.

Economic realities

A well-designed levy limit should allow local governments to increase revenue in line with broader economic realities, such as inflation and population growth.

While some levy limits use a fixed rate cap as a proxy for inflation — Massachusetts’ Proposition 2½, for example, uses a 2.5 percent annual growth factor — tying the formula directly to the prior year’s inflation rate would more closely align allowable revenue growth with legitimate fiscal need.

Accurate inflation adjustments help local governments maintain purchasing power as operating costs rise over time.

While it may intuitively make sense to use population growth as the second major component of the formula, in practice, new construction is a more effective variable because it directly expands the property tax base.

New homes and commercial development often bring additional service demands alongside additional taxable value, making new construction a practical proxy for population growth.

New construction

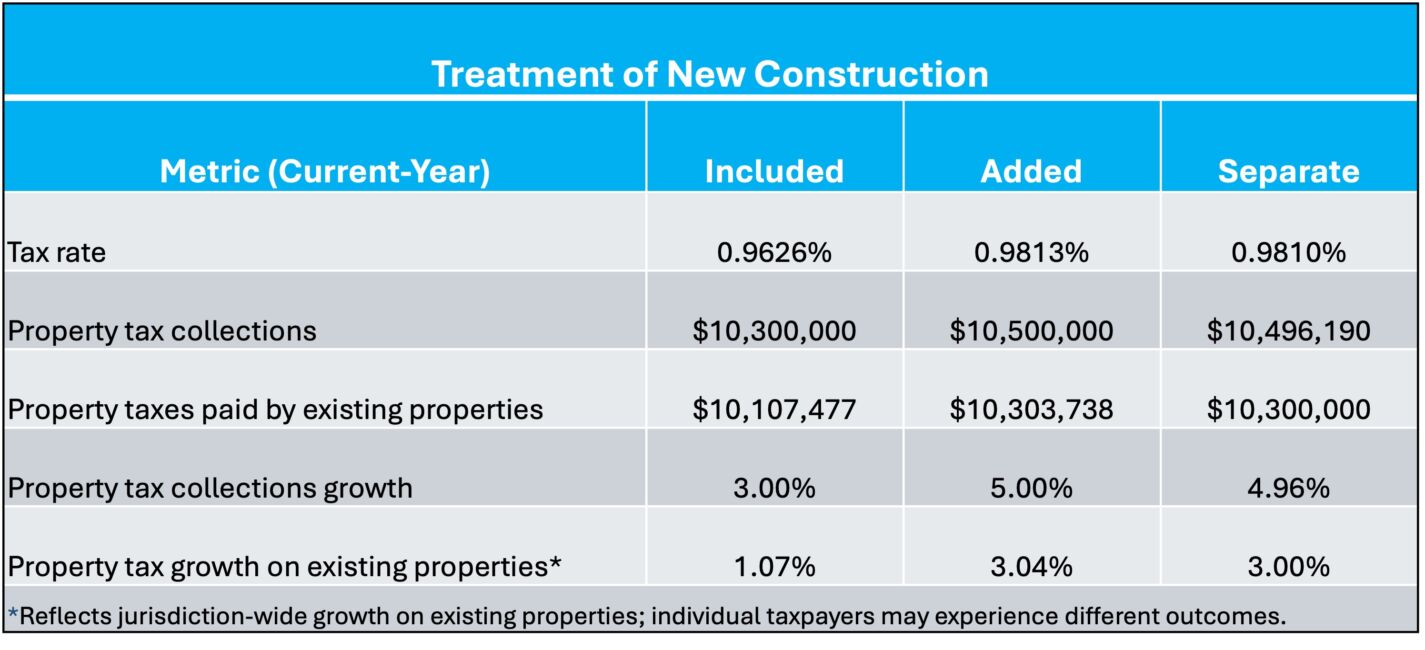

How a levy limit treats new construction is one of its most important design choices.

Consider the following example:

- Prior-year property tax base = $1 billion

- Prior-year property tax rate = 1%

- Prior-year property tax collections = $10 million

- Inflation adjustment = 3%

- Existing property values increase by 5%

- New construction expands the property tax base by 2%

In the “Included” model, revenue from new construction remains entirely within the levy limitation, meaning growth does not generate additional allowable revenue beyond the inflation adjustment itself.

In the “Added” model, revenue associated with new construction is added directly to the allowable levy using the prior year’s tax rate rather than the current year’s lower rate. As a result, when the total allowable levy is distributed across the expanded tax base, growth in new construction slightly increases the effective tax burden on existing property owners beyond the inflation adjustment.

In the “Separate” model, new construction is taxed separately at the current year’s rate, as applied to existing property. The annual levy limit would therefore only count revenue from pre-existing property. Under that framework, total collections still grow alongside new construction, but the additional revenue comes directly from the newly expanded tax base itself. This means that existing property owners only pay for the inflation adjustment.

Treating new construction separately would be best for North Carolina.

Minimal exceptions

A well-designed levy limit should apply broadly across property tax collections to prevent loopholes that undermine the policy’s purpose. Excessive carveouts and exemptions could weaken the effectiveness of the limit and encourage governments to shift revenue growth into excluded categories. Simply put, if it is a tax on real property paid by citizens within the jurisdiction, it should be subject to the cap.

Voter-approved overrides

Local governments should retain the ability to exceed the levy limit, but any such increases should require direct voter approval rather than be automatically implemented through the normal budget process. Override mechanisms help preserve flexibility while still maintaining accountability.

Taken together, these principles can help create a levy limit that prevents rapid increases in property tax collections during housing booms while still allowing local governments to generate sufficient revenue to fund public schools and public safety.

What still needs to be done?

With House Bill 1089 now receiving the constitutionally required three-fifths supermajority support in both the House and Senate, the proposal will appear before North Carolina voters as a constitutional amendment on the November ballot. At that point, a simple majority of voters will determine whether the amendment is adopted.

However, even if approved by voters, the real policy work will only begin afterward. Lawmakers will still need to pass accompanying legislation that defines the actual levy limit formula, including how inflation is measured, how new construction is treated, the override mechanisms, and which exceptions, if any, should apply.

Those details will ultimately determine whether North Carolina adopts a levy limit that provides meaningful taxpayer protections while still allowing local governments to respond to legitimate economic realities.

As a starting point for that discussion, the following model legislation attempts to operationalize the key principles identified above, including inflation-based growth adjustments, separate treatment of new construction, minimal exceptions, and voter-approved overrides.

Model legislation

SECTION 1. Property Tax Levy Limit.

(a) Except as otherwise provided by law, the total amount of ad valorem property tax revenue levied on existing real property by a local government for a fiscal year shall not exceed the prior fiscal year’s levy on existing real property multiplied by one plus the percentage change in the Consumer Price Index for All Urban Consumers (CPI-U) over the preceding calendar year.

(b) The assessed value attributable to new construction added to the real property tax base after the prior fiscal year shall be excluded from the levy limitation established under subsection (a) and calculated separately.

(c) After determining the allowable levy under subsection (a), a local government shall apply the resulting tax rate to the assessed value attributable to new construction, and the resulting revenue may be added to the local government’s total allowable property tax collections for the fiscal year.

(d) “New construction” shall mean the increase in taxable real property value attributable to new construction, improvements, and all other physical expansions of the real property tax base occurring after the prior year’s assessment roll.

(e) The levy limitation established under this section shall apply broadly to all ad valorem taxes levied on real property unless specifically exempted by general law.

(f) A local government may exceed the levy limitation established under this section only upon approval by a majority of qualified voters in a referendum held pursuant to general law.

(g) The General Assembly may enact general laws establishing procedures, enforcement mechanisms, calculation methodologies, and limited exceptions necessary to administer this section.