Provider taxes are levied on hospitals’ net patient revenues and used to fund the state’s 10 percent share of Medicaid expansion costs, helping draw down federal matching funds that support the program.

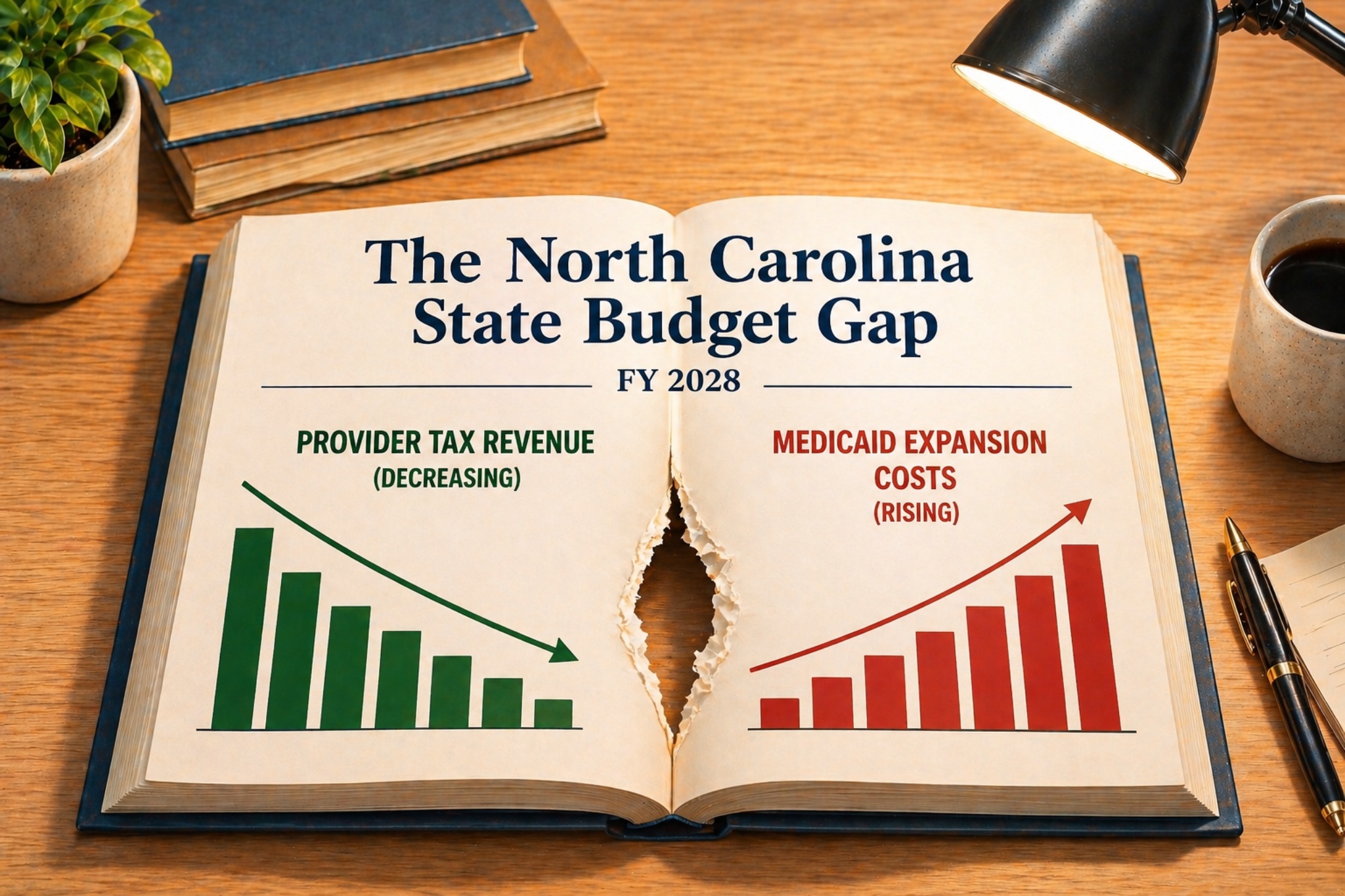

A provision in last year’s “One Big Beautiful Bill Act” mandates that beginning in 2028, the maximum provider tax rate states are allowed to charge will be reduced from 6 percent to 3.5 percent in annual decreases of 0.5 percentage points. This federal policy change is expected to create a growing gap between the cost of coverage for North Carolina’s Medicaid expansion population and available revenue.

Yet despite the fiscal implications, there has been limited public discussion of how these changes will affect the state’s budget. To better understand the potential magnitude of this issue, this analysis uses a model grounded in current enrollment, per-enrollee costs, and provider tax assumptions. In addition, this analysis evaluates policy reforms that could reduce the projected revenue gap.

Given the limited availability of publicly reported data on provider tax rates and net patient revenues, the model should be viewed as a rough map rather than a mirror. In other words, this is an exploratory framework intended to illustrate direction and scale rather than precise outcomes.

Model assumptions and inputs

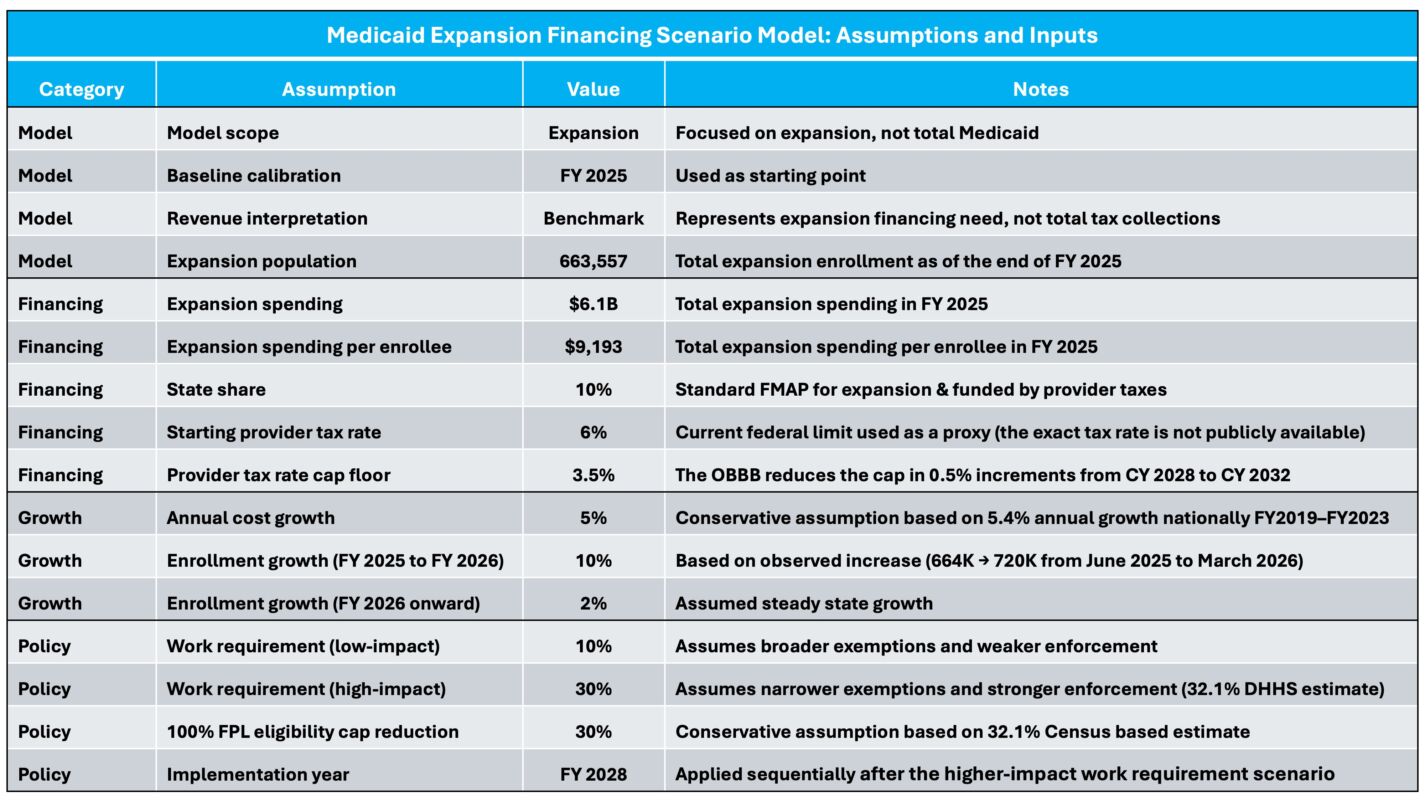

To provide a transparent foundation for the analysis, the table below outlines the key assumptions and inputs used in the model. The analysis is anchored in fiscal year (FY) 2025 expansion data and projects forward using conservative assumptions for enrollment and cost growth.

On the financing side, the model assumes a starting provider tax rate of 6 percent, the current federal upper limit. Because the tax rate is not publicly reported and may be lower in practice, this assumption is used as a proxy for the current financing environment. If the actual rate is below 6 percent, the timing and magnitude of the projected gaps would be reduced, with impacts occurring later and at a smaller scale.

Additional details, including the full model structure and calculations, are provided in the accompanying spreadsheet at the bottom of the article.

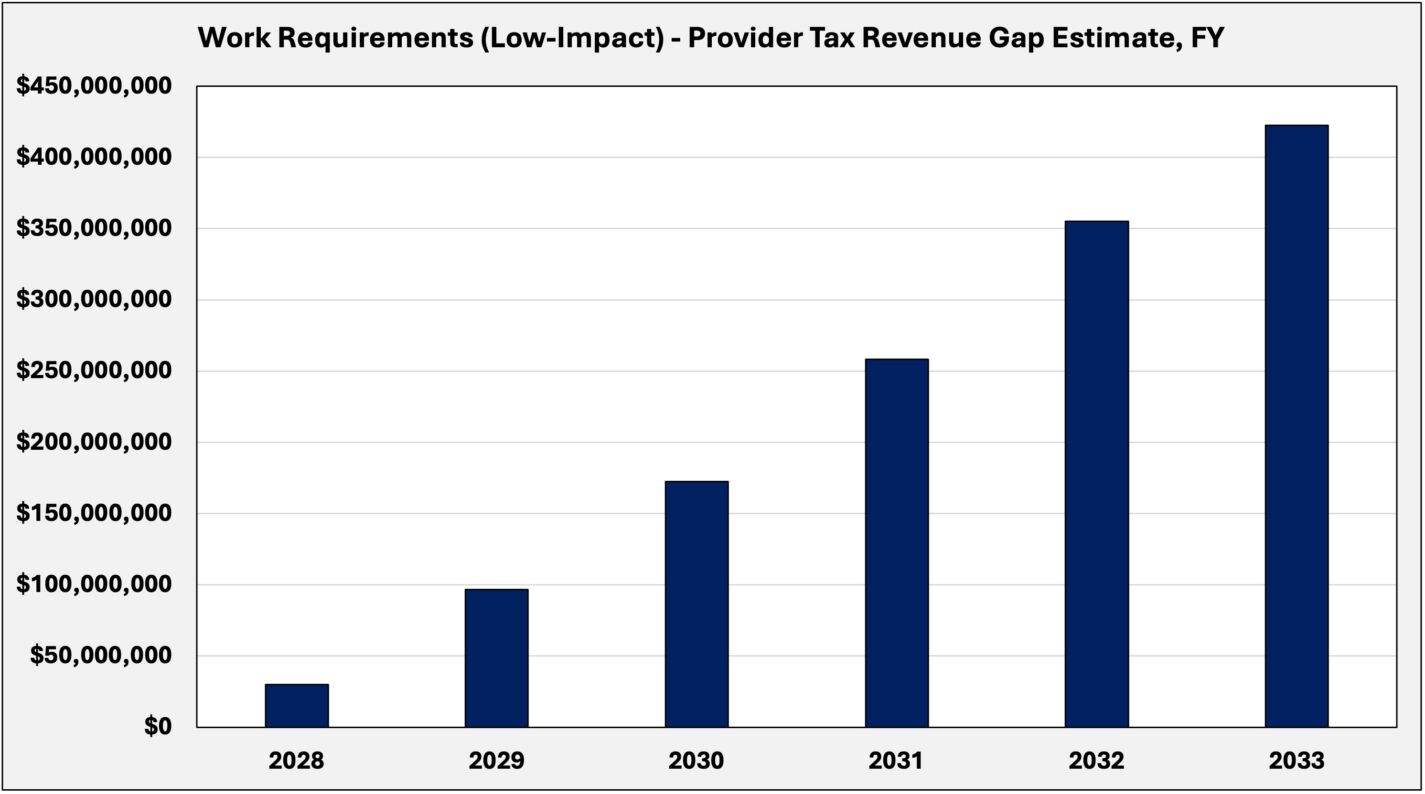

Work requirements (low-impact)

This scenario models the effect of declining provider tax capacity under a low-impact implementation of federal work requirements that take effect in 2027. While the policy is federally mandated, its practical effect depends on how exemptions — particularly the “medically frail” category — are defined and administered.

Under this scenario, enrollment declines modestly by 10 percent, reflecting a passive implementation approach in which exemptions are defined broadly, and enforcement is limited in the absence of additional legislative direction.

The annual shortfall rises from approximately $30 million in FY 2028 to about $422 million by FY 2033, as the allowable state provider tax rate falls. Over this period, the cumulative gap is roughly $1.34 billion.

It is important to note that this gap reflects only the state’s share of expansion costs. Because Medicaid expansion is financed with a 90 percent federal match, any shortfall not covered by the state would also result in a loss of federal funds. In practice, however, the state could avoid this outcome by funding its share of the gap.

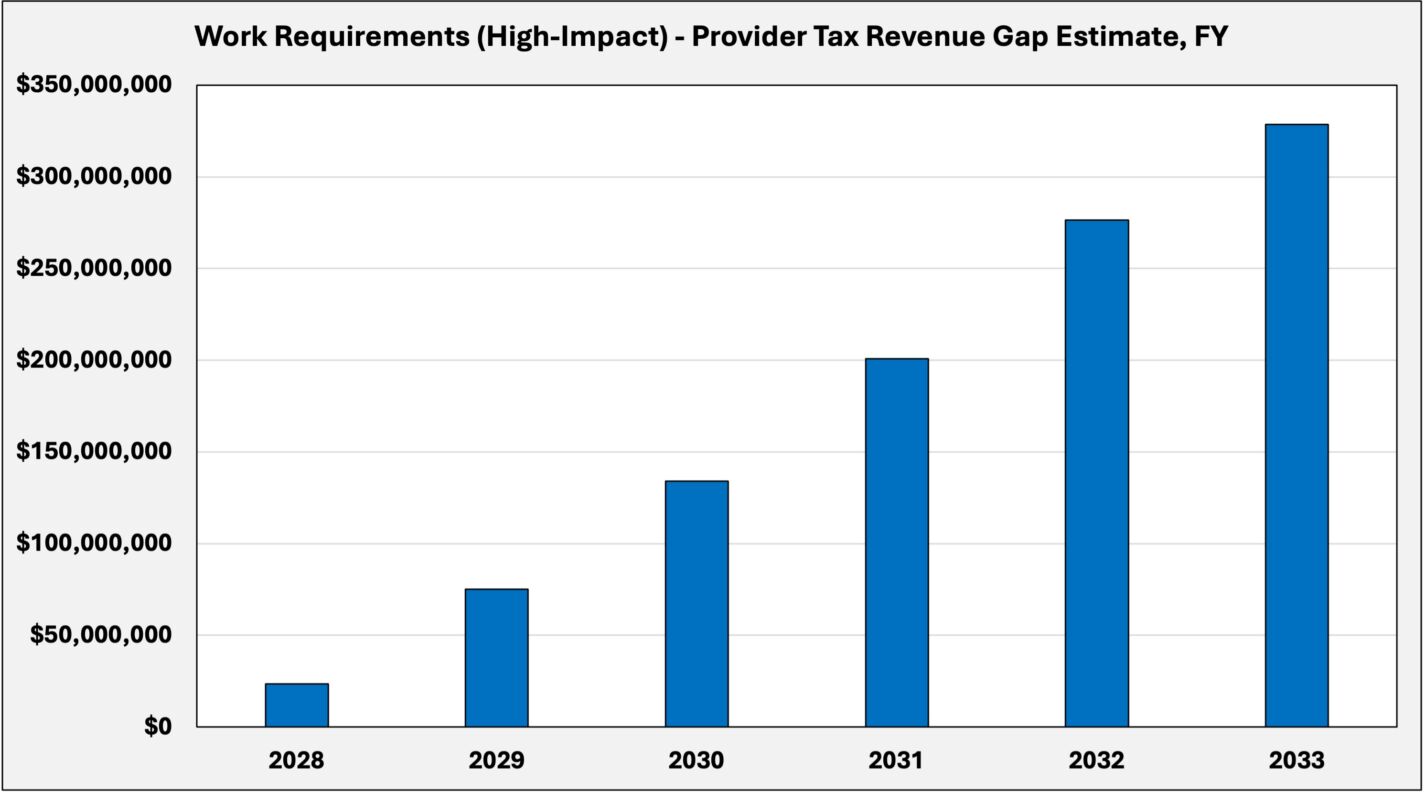

Work requirements (high-impact)

This scenario models a high-impact implementation of federal work requirements beginning in 2027. While many populations are explicitly exempt under federal guidelines, the definition of “medically frail” must be determined by the General Assembly.

A narrower definition delivered through legislative action, combined with more rigorous administrative enforcement, results in a larger share of the expansion population being subject to the requirement. Based on a prior North Carolina DHHS estimate, the scenario assumes a 30 percent reduction in enrollment.

This reduction lowers total spending and meaningfully reduces the projected financing gap. The annual shortfall in FY 2028 declines to approximately $23 million, compared to $30 million under the low-impact scenario. Over this period, the cumulative gap is reduced from $1.34 billion to approximately $1.04 billion.

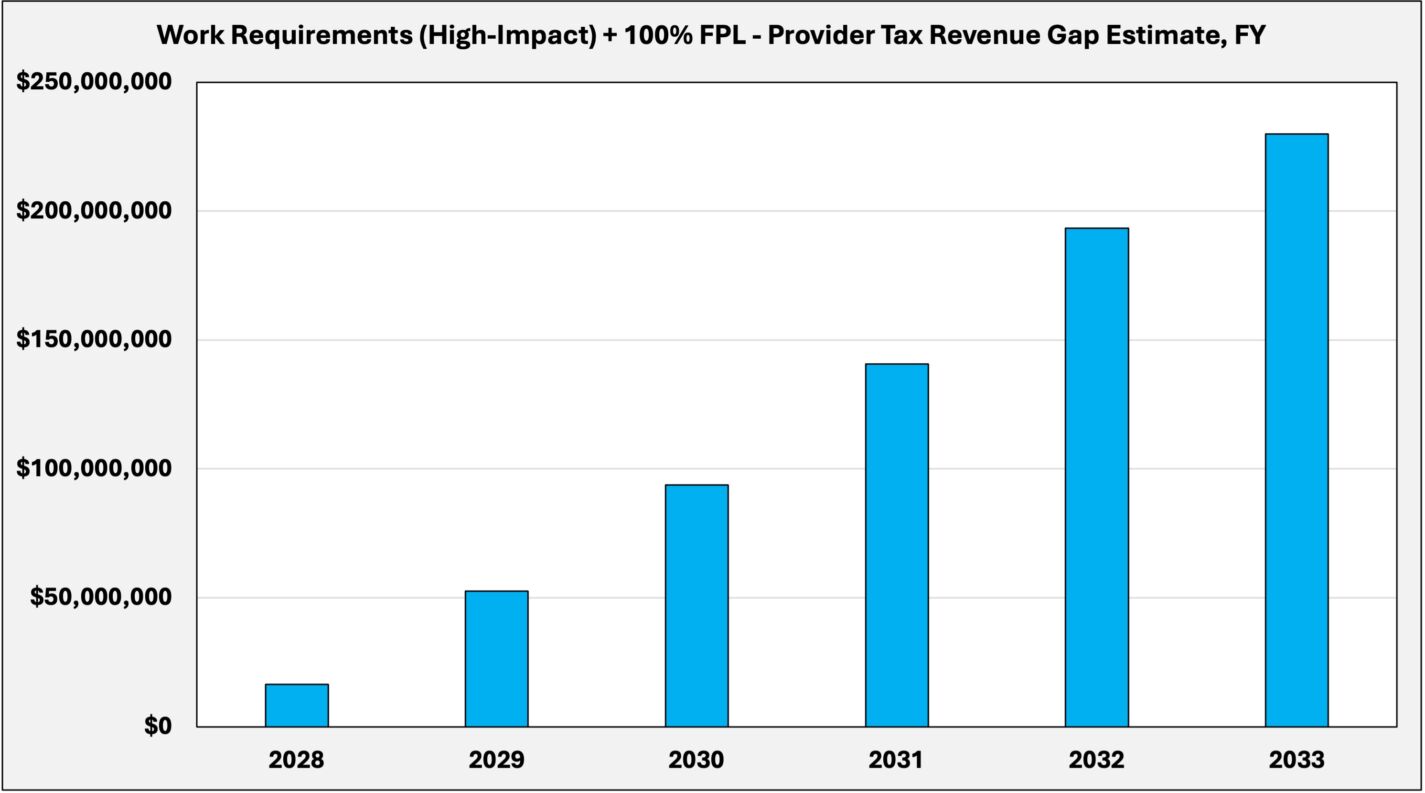

Work requirements (high-impact) and the 100 percent federal poverty level limit model

The third scenario builds on the prior model by combining high-impact work requirements with a tightening of income eligibility from 138 percent to 100 percent of the federal poverty level for the expansion population, which would require a waiver from the federal government. Based on state income data from the Census Bureau, this would result in an additional 30 percent enrollment reduction.

This combined approach further reduces total spending and lowers the projected financing gap. The annual shortfall in FY 2028 declines to approximately $16 million, compared to $30 million under the low-impact scenario. Over this period, the cumulative gap is reduced from $1.34 billion to approximately $727 million.

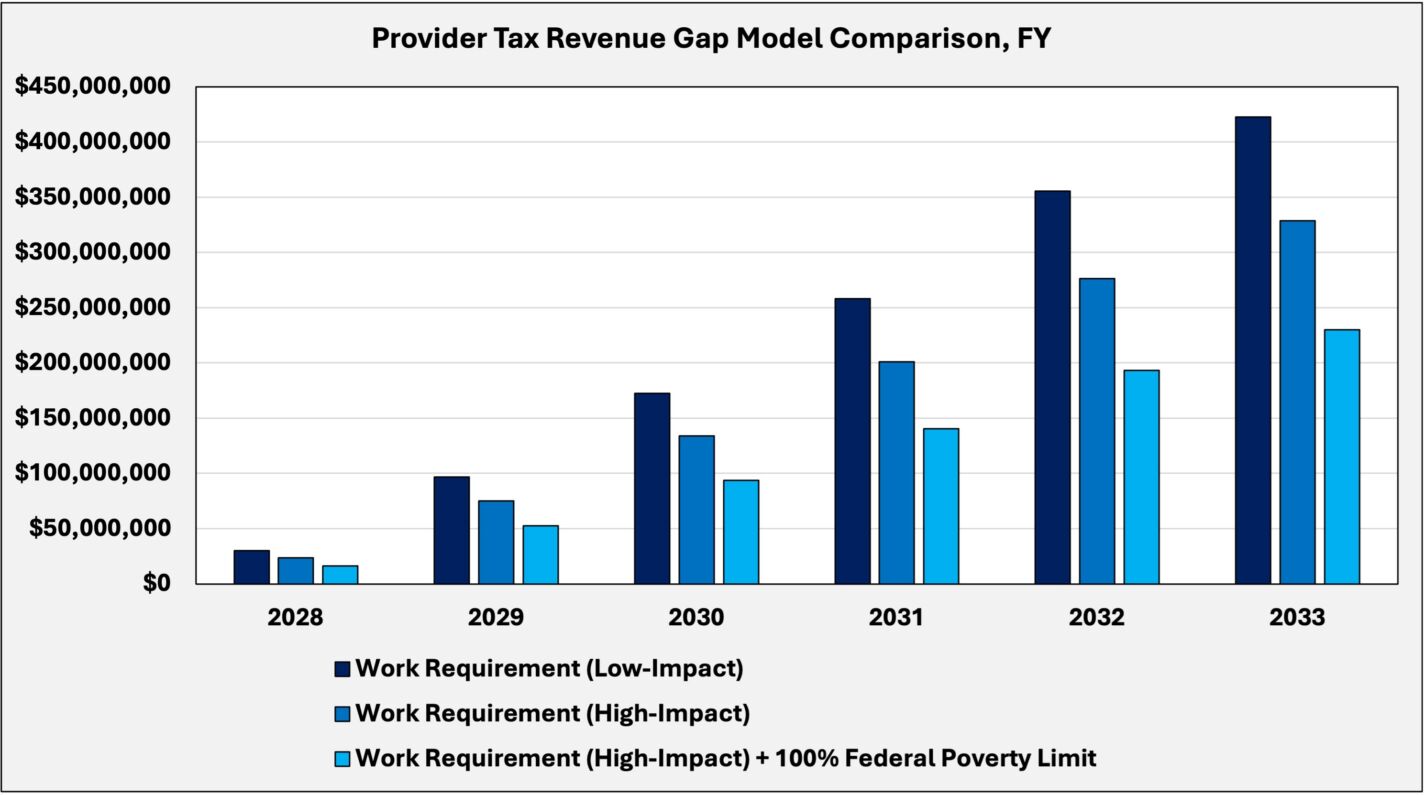

Model comparison

The results show that policy changes can meaningfully reduce the gap, with more aggressive reforms producing larger reductions.

Under low-impact work requirements, the gap reaches approximately $422 million in FY 2033. Implementing high-impact work requirements reduces this to about $329 million, while combining them with a 100 percent federal poverty-level eligibility cap further narrows the gap to roughly $230 million.

These differences reflect the direct impact of eligibility changes on total expansion spending. As enrollment declines, total program costs fall, thereby reducing the size of the state’s 10 percent share and the resulting financing gap.

Now is the time to act

Federal changes to provider tax policy will place increasing pressure on North Carolina’s current approach to financing Medicaid expansion.

Policymakers have several options. The General Assembly could allow the original trigger provision to take effect and repeal expansion if the financing structure fails, eliminating the gap but ending coverage for hundreds of thousands in the expansion population.

Alternatively, the state could maintain the program and absorb the fiscal impact through higher taxes or spending reductions elsewhere, such as slower compensation growth for teachers and state employees.

While the state currently has $500 million in the Medicaid Contingency Reserve, the legislature has approved a bill to draw down $319 million of those funds to pay for this year’s rebase. This would leave a relatively small amount to address the future gap and would be exhausted quickly.

Reforms, such as strictly implementing work requirements and lowering the income eligibility cap, can meaningfully reduce the size of the gap. However, these policy choices require timely action and clear legislative direction.

Given these realities, the General Assembly should act this session to prepare for the coming changes. At a minimum, policymakers should direct a formal analysis of the state’s Medicaid expansion financing structure, including greater transparency around provider tax rates and the underlying net patient revenue tax base. Without this information, it is difficult to adequately assess the scope of the problem.

The timeline for federal changes is already underway. The question is not whether the state will need to respond, but how — and whether that response will be proactive or reactive.